|

|

发表于 29-1-2008 01:07 PM

|

显示全部楼层

发表于 29-1-2008 01:07 PM

|

显示全部楼层

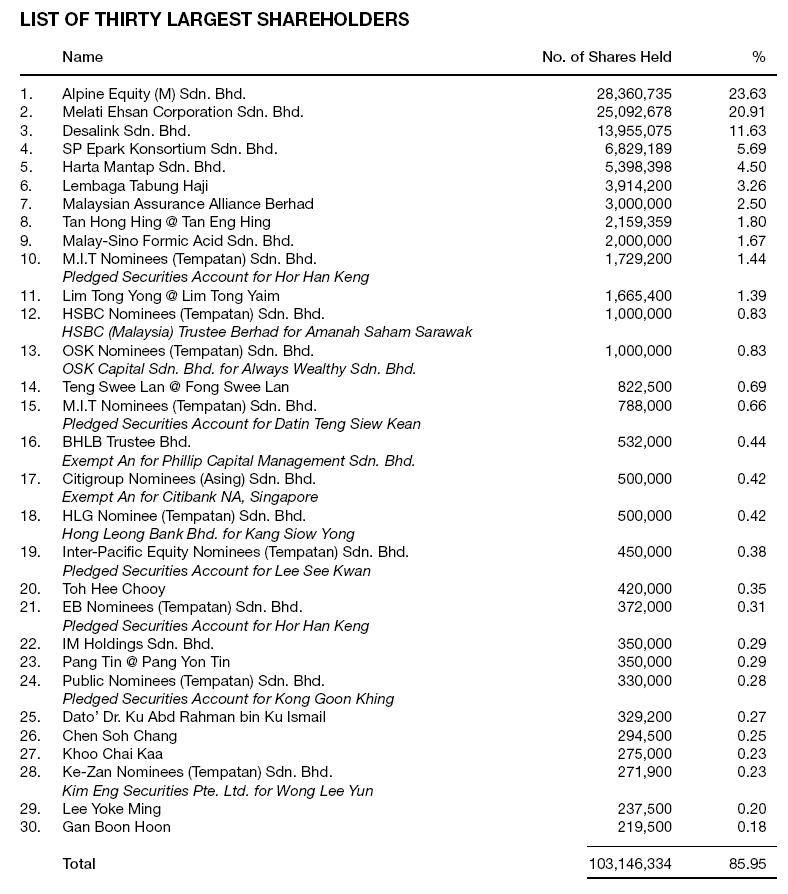

30大股东就控制了Melati的85.95%股份。。。

PS: 很意外,原来有蛮多基金是Melati的股东。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 05:18 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 05:33 PM

|

显示全部楼层

让人失望的财报。。。。。。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 05:35 PM

|

显示全部楼层

| Listing Circular | | LISTING'S CIRCULAR NO. L/Q : 48436 OF 2008 |

| Company Name | : | MELATI EHSAN HOLDINGS BERHAD | | Stock Name | : | MELATI | | Date Announced | : | 29/01/2008 |

| Subject | : | | MELATI - NOTICE OF BOOK CLOSURE |

|

| | Contents | : | A first and final dividend of 7.5 sen per share less 26% tax.

Kindly be advised of the following :

1) The above Company's securities will be traded and quoted [ "Ex - Dividend" ]

as from : [ 28 February 2008 ]

2) The last date of lodgement : [ 3 March 2008 ]

3) Date Payable : [ 19 March 2008 ] |

|

[ 本帖最后由 Mr.Business 于 29-1-2008 05:36 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 05:35 PM

|

显示全部楼层

| Financial Results | | Reference No CS-080128-61991 |

| Company Name | : | MELATI EHSAN HOLDINGS BERHAD | | Stock Name | : | MELATI | | Date Announced | : | 29/01/2008 |

| Financial Year End | : | 31/08/2008 | | Quarter | : | 1 | | Quarterly report for the financial period ended | : | 30/11/2007 | | The figures | : | have not been audited |

| Please attach the full Quarterly Report here: |

MEHB-FinancialStt.xls MEHB-FinancialStt.xls

MEHB-Notes.doc

As this is the fourth quarterly report being drawn out after theGroup was conceived on 3 January 2007, there are no comparativeconsolidated figures for the preceding financial year's correspondingquarter and period to-date.

SUMMARY OF KEY FINANCIAL INFORMATION | 30/11/2007 |

| INDIVIDUAL PERIOD | CUMULATIVE PERIOD | | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | | 30/11/2007 | 30/11/2006 | 30/11/2007 | 30/11/2006 | | RM'000 | RM'000 | RM'000 | RM'000 | | 1 | Revenue | 39,537 | 0 | 39,537 | 0 | | 2 | Profit/(loss) before tax | 5,468 | 0 | 5,468 | 0 | | 3 | Profit/(loss) for the period | 4,109 | 0 | 4,109 | 0 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 4,109 | 0 | 4,109 | 0 | | 5 | Basic earnings/(loss) per share (sen) | 3.42 | 0.00 | 3.42 | 0.00 | | 6 | Proposed/Declared dividend per share (sen) | 0.00 | 0.00 | 0.00 | 0.00 |

|

|

|

|

|

|

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent (RM) | 1.0000 | 0.9700 |

Note: For full text of the above announcement, please access Bursa Malaysia website at www.bursamalaysia.com

[ 本帖最后由 Mr.Business 于 29-1-2008 05:37 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 05:48 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 06:42 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 06:45 PM

|

显示全部楼层

|

因为通常第一季都会比较差,而第四季会是最好的一个quater。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 06:50 PM

|

显示全部楼层

|

RM0.0342 Q108 EPS (过去式) vs RM1.7billion orderbook (前瞻性) |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-1-2008 09:49 PM

|

显示全部楼层

管理层并没有欺骗投资者,只是我们太乐观。。。

last 4 qta

Review of performance

For the current quarter under review, the Group recorded profit from operations of RM13.959 million on the back of revenue of RM55.132 million. The Group recorded a profit before tax of RM13.958 million and a profit after tax of RM10.198 million, with increasing contracts in hand pushing order book to over the RM1.2 billion mark.

There were no comparative figures in the preceding financial year as this is the Group’s second quarterly announcement.

B2. Comparison with preceding quarter results

For the current quarter under review, the Group recognized for the full three (3) months while for the preceding quarter, the Group recognized two (2) months results as the Group was formed on 3 January 2007. For the current quarter under review, the Group recorded profit before tax of RM13.96 million compared to RM6.04 million in the preceding quarter due to rising contribution from infrastructure project such as the Laluan Persekutuan 54, Sungai Buloh (FR54). Work on the turnkey project to upgrade the FR54 was completed on time and handover is expected anytime soon. Profit growth for the current quarter was also driven by increased contribution from the property construction in the Taman Ehsan Jaya, Johor development.

这就是为什么我们会失望,事实上是我们看了一个最强的4qta来判断。所以对melati有必需降低期望,今年大概的eps会在17sen或22sen左右。目前pe应该在9左右。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-1-2008 12:12 AM

|

显示全部楼层

原帖由 8years 于 29-1-2008 06:45 PM 发表

因为通常第一季都会比较差,而第四季会是最好的一个quater。

8年兄,为什么通常第一季都会比较差?这个有根据吗? |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-1-2008 12:15 AM

|

显示全部楼层

原帖由 Mr.Business 于 29-1-2008 01:07 PM 发表

30大股东就控制了Melati的85.95%股份。。。

PS: 很意外,原来有蛮多基金是Melati的股东。

30大股东的第二位melati ehsan corp sdn bhd...请问生意兄,dato yap在这间私人公司(sdn bhd)的股份有多少?我还没看年报。。。最近比较忙。。。里面有讲到吗? |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-1-2008 12:30 AM

|

显示全部楼层

回复 311# 草下飞 的帖子

其实不是第一季比较差,而是第四季比较强。310写明去年4th qta强的原因是因为有几个project close,所以就有比较高的盈利,因为通常project是以progressive来payment,看情况,有时是30,30,40或30,20,50等等不同条件。

比如说第一季到第三季我们拿60,就是平均每季20。那么在第四季时就能拿40%,也就是比其他季高一倍,这就是为什么建筑工程在收到尾数时盈利特别高。

现在其实第一季才是真正反映了melati的普通赚钱能力(假如没有close project的话),接下来2,3如果没有close project的话应该也会有4sen到4.5sen。能够期望的是第四季close project时的盈利。所以预测大概会有.17sen到22sen左右。如果以17sen来算,现在差不多是8-9pe之间。。。。。。。。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-1-2008 12:36 AM

|

显示全部楼层

我刚刚又再看了去年ended 28feb的quarterly report,那时候的net profit和现在相差不远,其实还比现在少(因为negative goodwill提高了1million左右的net profit)。。。可是eps确有8sen左右。。。那是因为28feb以前的还未算入ipO的股票数量。。

到了第三、第四季。。。melati的eps 有明显增进,net profit 也大大提升。。。所以我同意8年兄说的,我们看到了强劲的Q3 & Q4。。。

现在08年第一季的业绩(ended 30 Nov 07)确实不理想,可是老实说,我还是乐观的,因为我相信业绩不能单凭一个季就去下定论。。。我们应该看全年还有更重要的是未来的动向。。既然melati有能力在去年赚取高的eps,我认为如果以他每年(历史现实,每年如此)最低30%投标成功率而言。。。melati今年的eps应该还是相当可观。。。否则,tabung haji也不会如此看好而买进。。。tabung haji 是政府基金之一,也许他知道的消息比外人知道得快。。当然,这只是我的猜测。。。

再说,能够发股息,增明公司是乐观的。。。因为公司要有利润才能发股息。所以虽然我有点失望,可是我整体还是看好melati。。除非它的业绩变坏了。。不然我还是会继续持有。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-1-2008 12:45 AM

|

显示全部楼层

回复 314# 草下飞 的帖子

|

我没有那么乐观,不过我赞同你讲的话。如果有谁有证券行的分析报告,请post上来和大家分享。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-1-2008 08:48 AM

|

显示全部楼层

原帖由 草下飞 于 30-1-2008 12:15 AM 发表

30大股东的第二位melati ehsan corp sdn bhd...请问生意兄,dato yap在这间私人公司(sdn bhd)的股份有多少?我还没看年报。。。最近比较忙。。。里面有讲到吗?

IPO资料有写,你可以去看看。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 31-1-2008 03:29 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 31-1-2008 03:36 PM

|

显示全部楼层

回复 317# 草下飞 的帖子

谢谢草下飞侠。

Slowly but Surely

As expected, 1Q results came in rather slow owing to seasonality factors. We expect things to pick up slightly in 2Q and accelerate in the last 2 quarters. Its strong orderbook balance of RM1.4bn should continue to drive earnings moving forward. The company has already tendered for over RM1bn worth of projects. Maintain BUY with a TP of RM2.35, citing a 57% upside.

Seasonally lower.

Melati registered a net profit of RM4.1m for 1QFY08, or 12.4% of our original full year forecast. Traditionally, 1H tends to be the weaker half attributed to

(i) rainy season hampering construction works and

(ii) the relative abundance of public holidays during the period.

We expect only a marginal pick up in the following quarter but things should kick back into high gear during Q3 and Q4. To reaffirm this seasonality effect, 1H earnings only made up 21% of its FY07 results.

Margins remain healthy.

Gross and net margins came in spot on at 15.9% and 10.4%, vis-à-vis our projection of 15.6% and 10.3%. We continue to like Melati’s ability to command such healthy margins even in light of rising raw material prices. To recap, most of its government awarded projects contain a “Variation of Price” clause, protecting

margins from adverse fluctuations in prices of key raw materials.

Property development – Minor setback.

We understand that the launch of its maiden property development in Pandamaran, Klang will be done in 2Q 2008 instead of 1Q. However, to maintain a conservative stance, we have now assumed that take up rates will only commence in FY09 (i.e. post Aug 2008). This property venture constitutes a mixed development comprising residential houses and shop lots with a total GDV of RM500m.

What next?

We understand that Melati has submitted a proposal to participate in the earthworks, infrastructure and drainage of a property development in Ijok, Selangor. The mixed development is being conducted by Kuala Lumpur Kepong Bhd (BUY, RM17.20) and is known as Desa Coalfield with a total land space of 1,500 acres. Further, Melati is also eyeing on some flood mitigation jobs located in Johor.

A value BUY.

We forecast an earnings growth of 15.5% and 29.3% for FY08 and FY09 respectively. Current multiples are very undemanding at 6.4x FY08 earnings and 5.0x FY09 earnings. Owing to its recently listed status, we tag a 9x multiple (rather than our standard 11x to 13x) to FY08 earnings. Maintain BUY with a target price of RM2.35.

[ 本帖最后由 Mr.Business 于 31-1-2008 03:50 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 31-1-2008 04:41 PM

|

显示全部楼层

|

这个公司有没有website?它吧生的project是在哪里? |

|

|

|

|

|

|

|

|

|

|

|

发表于 31-1-2008 06:16 PM

|

显示全部楼层

原帖由 草下飞 于 30-1-2008 12:36 AM 发表

除非它的业绩变坏了。。不然我还是会继续持有。

现在还不够坏吗?该丢鸟 |

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3235

3235  76

76