|

|

发表于 28-10-2015 03:58 PM

|

显示全部楼层

发表于 28-10-2015 03:58 PM

|

显示全部楼层

本帖最后由 icy97 于 28-10-2015 04:02 PM 编辑

美德再也 南非购地预料之外

财经 股市 行家论股 2015-10-28 10:44

http://www.nanyang.com/node/731092?tid=462

目标价:1.63令吉

最新进展

美德再也(MITRA,9571,主板建筑股)子公司Mitrajaya Development SA Proprietary,在南非的东北部城市比勒陀利亞(Pretoria)购买总面积215亩土地,总值4000万兰特(约1218万4000令吉)。

该公司计划发展16亿兰特(约4亿9800万令吉)的产业项目,然而目前处于初步阶段。

美德再也预计可在明年1月31日完成收购。

行家建议

我们对这项收购活动感到惊讶,因为我们预测该公司仅专注发展Blue Valley Gold & Country Estate(简称“BVGCE”)项目,该项目位于公司旗下南非300亩地块。

美德再也在南非拥有发展总值(GDV)达4亿令吉的BVGCE产业发展项目,从2010年动工,预计在近期竣工。

该公司计划发展共1600单位的Eco Park住宅产业项目,估计发展总值为16亿兰特。

在本财年次季,美德再也负债率为0.23倍,我们预估完成收购后将会提升至0.26倍,但仍在0.5倍内的舒适范围。

根据过往的表现,我们预测这项发展项目能达到扣除利息和税务前盈利(EBITDA)赚幅35至40%,与BVGCE项目的38%相似。虽然这项收购料于明年首季完成,但美德再也不会在短期内开始动工。

分析: 肯纳格研究 |

|

|

|

|

|

|

|

|

|

|

|

发表于 19-11-2015 12:47 AM

|

显示全部楼层

本帖最后由 icy97 于 19-11-2015 02:09 AM 编辑

Double COMBO: GADANG vs MITRA

Author: Gainvestor10sai | Publish date: Tue, 17 Nov 2015, 11:45 PM

http://klse.i3investor.com/blogs/gainvestor10sai.blogspot.com/86319.jsp

In my previous post, i talk about the impact of Malaysia Budget towards our FBMKLCI and also construction index. I monitor these 2 counters for past few weeks. The magic might be happening already. (Refer to my previous post on my view of Malaysia Budget 2016 towards our equity market,

Let us look at the construction index. There is a cup with handle and the breakout point at 271.42, with a resistance at 284. With the budget announcement coming, perhaps it will challenge the resistance. If the market sentiment is positive, then, it should not be a problem overtaking the 284.

In this post, i gonna roughly going through 2 construction counters, namely GADANG and MITRA. If our Budget 2016 is not disappointing, i think there will be another round of breakout for the construction counters.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-11-2015 12:51 AM

|

显示全部楼层

quarterly results应该这几天吧?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-11-2015 06:23 PM

|

显示全部楼层

今天还不错

1.28 +0.07 (5.79%)

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2015 05:57 PM

|

显示全部楼层

本帖最后由 icy97 于 3-12-2015 03:02 PM 编辑

美德再也获国油1.86亿合约

财经新闻 财经 2015-11-27 10:08

http://www.nanyang.com/node/736104?tid=462

(吉隆坡26日讯)美德再也(MITRA,9571,主板建筑股)获颁边佳兰炼油与石油化工综合发展(RAPID)工程的相关合约,总值1亿8638万1642令吉。

根据文告,该公司是通过独资子公司美德再也建筑私人有限公司(PMJ) 和Ismail Ibrahim私人有限公司(SII)组成的财团,获得国油子公司PRPC公用事业和设施颁发该项合约。

根据合约,该公司将负责公用设施第1区(Utilities Area 1 )的土木和建筑工程的采购、建筑和测试。

同时,公司也将为国油石化共享区(PetChem Commons Area)提供连接、排洪和公用设施的服务。

次季净利涨70%

另一方面,美德再也截至6月30日次季业绩报捷,归功于建筑业务和南非投资的盈利贡献走高。

该公司次季净利按年增70.07%,至2309万4000令吉,超越去年同期的1357万9000令吉。

营业额则按年攀涨80.53%,从1亿3471万9000令吉增至2亿4320万5000令吉。

累积首半年,净利按年涨幅48.88%,报3648万7000令吉;营业额则上扬69.45%,达4亿479万8000令吉。

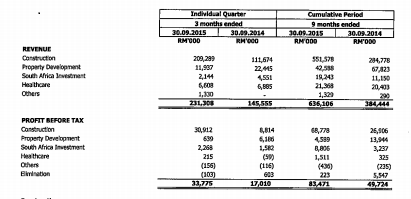

SUMMARY OF KEY FINANCIAL INFORMATION

30 Sep 2015 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 30 Sep 2015 | 30 Sep 2014 | 30 Sep 2015 | 30 Sep 2014 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 231,308 | 145,555 | 636,106 | 384,444 | | 2 | Profit/(loss) before tax | 33,918 | 17,010 | 83,625 | 49,724 | | 3 | Profit/(loss) for the period | 25,873 | 12,928 | 62,455 | 37,196 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 25,821 | 13,117 | 62,308 | 37,624 | | 5 | Basic earnings/(loss) per share (Subunit) | 4.08 | 2.22 | 10.06 | 6.36 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.7300 | 0.9900

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2015 10:37 PM

|

显示全部楼层

本帖最后由 icy97 于 26-11-2015 02:54 AM 编辑

a) QoQ increase 70%

b) Award project

c) Share Buy Back

双喜临门。希望喜事可以反央在股价上

Type | Announcement | Subject | OTHERS | Description | Mitrajaya Holdings Berhad ("MHB" or the "Company")Consortium of Pembinaan Mitrajaya Sdn Bhd ("PMJ") and Syarikat Ismail Ibrahim Sdn Bhd ("SII")awarded contract for Refinery and Petrochemicals Integrated Development ("RAPID") Project inPengerang, Johor | The Board of Directors of Mitrajaya Holdings Berhad (“MHB” or the “Company”) is pleased to announce that its wholly owned subsidiary, Pembinaan Mitrajaya Sdn Bhd (“PMJ”) and Syarikat Ismail Ibrahim Sdn Bhd (“SII”) as a consortium has been awarded a contract for the procurement, construction and commissioning (“PCC”) of civil, and infrastructure works at Utilities Area 1 (Package 14-0304) and Petchem Commons Area (Package 14-0305) for interconnecting, storm water drainage and utilities for the RAPID project (“the Contract”). The Contract, dated 19 November 2015, was awarded by PRPC Utilities and Facilities Sdn. Bhd (“Project Owner”) for a contract sum of RM186,381,642.06.

PMJ had entered into a joint venture agreement with SII on 3 April 2015 (“JV”) for the purpose of submitting a tender for the construction of the Contract with PMJ’s participating interest in the JV being 51%.

Under the contract, the duration of Package 14-0304 and Package 14-0305 is 32 months and 22 months respectively from contract award date.

The Contract is expected to contribute positively to MHB Group’s future earnings.

None of the Directors or major shareholders of the Company and persons connected with such directors or major shareholders have any interest in the Contract.

This announcement is dated 25 November 2015. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2015 10:45 PM

|

显示全部楼层

本帖最后由 icy97 于 25-11-2015 11:05 PM 编辑

Mitrajaya's 3Q net profit surges 97% on higher construction contribution

By Ahmad Naqib Idris / theedgemarkets.com | November 25, 2015 : 7:00 PM MYT

http://www.theedgemarkets.com/my/article/mitrajayas-3q-net-profit-surges-97-higher-construction-contribution

KUALA LUMPUR (Nov 25): Mitrajaya Holdings Bhd ( Valuation: 2.00, Fundamental: 1.50)'s net profit surged 97% to RM25.82 million or 4.08 sen per share for the third quarter ended Sept 30, 2015 (3QFY15) from RM13.12 million or 2.22 sen per share a year earlier.

Revenue for the quarter soared 59% to RM231.31 million from RM145.56 million in the previous year.

In a filing with the exchange, Mitrajaya said the significantly better performance for the quarter was due to higher contribution from the construction division and its South Africa investment.

"The construction division was the major contributor to the increase in group revenue and profit before tax. It was attributable to the higher recognition from new projects secured since last year," it said.

While its South Africa investment saw lower revenue year-on-year, the division saw higher profit, attributed to better net profit margin of stands sold.

Meanwhile, its property development saw lower revenue and profit contribution during the quarter, while its healthcare segment had turned around and posted profit, despite a decline in revenue.

For the nine months ended Sept 30 (9MFY15), net profit jumped 66% to RM62.31 million from RM37.62 million in 9MFY14, while revenue was up 65% at RM62.31 million compared to RM37.62 million in the previous year.

Going forward, Mitrajaya expects strong performance for FY15, driven by its construction division and its investment in South Africa.

"The construction division will contribute significant high revenue and profit before tax for FY15, as works of the existing ongoing project [are] progressing well from the current outstanding orderbook of RM1.39 billion.

"Our investment in South Africa is also expected to record significant growth in revenue and profit for FY15. The unbilled sales currently stands at Rand 40 million (RM11.98 million), which will be recognised progressively by end of this year," said the group.

However, it expects weaker performance for its property division, as its ongoing Wangsa 9 Residency project is undergoing its initial stage of construction.

In a separate statement, Mitrajaya announced that its wholly-owned subsidiary Pembinaan Mitrajaya Sdn Bhd (PMJ) and Syarikat Ismail Ibrahim Sdn Bhd (SII) as a consortium was awarded a construction contract relating to the Refinery and Petrochemical Integrated Development (RAPID) project worth RM186.38 million.

The contract, awarded by PRPC Utilities and Facilities Sdn Bhd, entails the procurement, construction and commissioning of civil and infrastructure works at Utilities Area 1 (Package 14-0304) and Petchem Commons Area (Package 14-0305) for interconnecting, storm water drainage and utilities for the RAPID project.

"Under the contract, the duration of Package 14-0304 and Package 14-0305 is 32 months and 22 months respectively from contract award date. The contract is expected to contribute positively to Mitrajaya group's future earnings," it said.

To recap, PMJ had entered into a joint venture (JV) with SII on April 3 to tender for the contract. PMJ holds a 51% stake in the JV.

Shares in Mitrajaya fell three sen or 2.4% to close at RM1.22, giving a market capitalisation of RM802 million.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2015 09:14 AM

|

显示全部楼层

本帖最后由 icy97 于 26-11-2015 03:53 PM 编辑

【美德显威】- MITRA(9571)再创佳绩,盈利yoy进步了97%!

Wednesday, November 25, 2015

http://harryteo.blogspot.tw/2015/11/1172-mitra9581.html

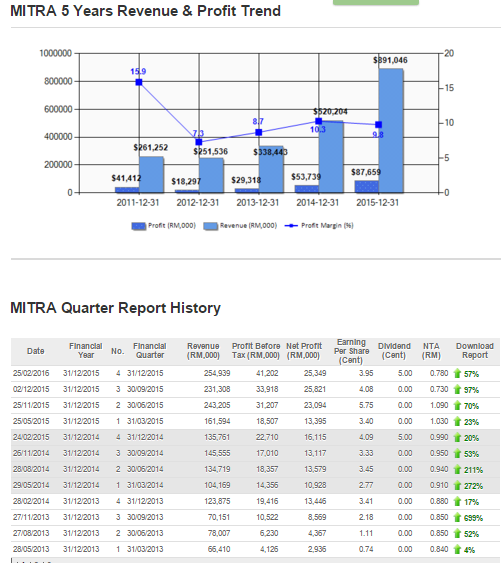

MITRA是一家成长非常惊人的建筑公司,公司的盈利很给力地连续进步了11个Quarter。而MITRA最新一季的盈利进步了97%,而EPS则进步了83.7%。这个季度的盈利是25.821mil,也是这家建筑公司的历史新高。现在的EPS为12.22, PE是9.98,而ROE更是来到了16.97的水平!

而最新的业绩显示,建筑领域还是最大的贡献者,占了公司Profit before Tax的91.5%。虽然南非投资的营业额下跌,但是盈利的Profit Margin增加导致yoy持续进步,这个季度的税前盈利是2.268 mil,占了总盈利的6.71%。而产业领域也一如预期,盈利继续下滑,盈利只有区区的0.639 mil。

公司截至9月30日,公司手上还有13.9亿的建筑合约。还有10月9号的52mil的合约,加上今天跟SII合作拿到RAPID的183mil合约,持有51%的MITRA应该会获得92 mil的合约。总额来说,MITRA现在一共有15.3亿左右的合约。此外,公司现在还在竞标着新的合约,希望会陆续有好消息传来。

最后,公司在南非还有大约11.98 mil未进账销售,相信会在年底结账。管理层相信2015年会是很杰出的一年,因为MITRA的传统旺季都是在Q4. 之前管理层说今年有信心达到10亿的营业额,现在大约是6.36亿,不知道第4个季度会不会有惊喜呢??其实只要Q4有2.6亿左右的营业额就已经突破单季历史新高了,让我们拭目以待吧。

魔法师Harryt30

21.42p.m.

2015.11.25 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-12-2015 04:33 PM

|

显示全部楼层

发表于 22-12-2015 04:33 PM

|

显示全部楼层

建筑订单支撑双数增长 美德再也明年放眼10亿合约

财经新闻 财经 2015-12-22 14:08

(吉隆坡21日讯)目前在国内竞标着48亿令吉建筑合约的美德再也(MITRA,9571,主板建筑股),放眼在2016财年能赢得总值10亿令吉的合约。

该公司估计,有建筑订单的支撑,下财年能持续达到双位数增长。

董事经理陈永标接受《The Edge》财经日报访问时指出,由于房市仍处于疲弱,因此建筑业务将是公司主要的盈利动力。

他预计建筑领域在明年仍持续走强,因许多大型项目陆续推出,如捷运工程(MRT)和泛婆罗洲大道(Pan Borneo Highway)。

“公司积极的竞标新工程,包括基建和混合建筑,下财年的目标是能赢得10亿令吉的合约。”

他披露,公司冀望在年底前能赢得多一两项合约。鉴于合约尚未颁发,因此目前难以公布相关的资料。

美德再也目前手握14亿8000万令吉的合约,足以支撑未来2年的盈利。

陈永标估计,可在今财年维持盈利增长,同时相信在下财年有望维持双位数增长。

尽管房市仍低迷,但对业绩冲击不大,因产业发展仅占总营业额的11%。建筑产业则贡献86%,其余3%由保健贡献。

美德再也目前专注在大马和南非市场,持续在这两个国家物色更好展望的商机。

鉴定Optimax买家

另一方面,该公司脱售Optimax眼科中心51%股权的计划,目前仍在鉴定买家,估计可在明年的首季或次季完成交易。

陈永标说,目前有数个买家有意购买,不过交易尚未敲定,因此未能公布更多的详情。【南洋网财经】 |

|

|

|

|

|

|

|

|

|

|

|

发表于 6-2-2016 06:03 AM

|

显示全部楼层

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

RELATED PARTY TRANSACTIONS | Description | MITRAJAYA HOLDINGS BERHAD (MITRAJAYA or COMPANY)PROPOSED DIVESTMENT BY MITRAJAYA OF 1,275,000 ORDINARY SHARES OF RM1.00 EACH, REPRESENTING 51% EQUITY INTEREST IN OPTIMAX EYE SPECIALIST CENTRE SDN. BHD. (OPTIMAX) FOR CASH CONSIDERATION OF RM5.1 MILLION (PROPOSED DIVESTMENT) | The Board of Directors of Mitrajaya wishes to inform that the Company had on 5 February 2016 entered into a Sale and Purchase of Shares Agreement with Optimax Healthcare Services Sdn. Bhd. (“the Purchaser”) to divest 1,275,000 ordinary shares of RM1.00 each in Optimax (“Sale Shares”) to the Purchasers for a cash consideration of RM5,100,000.00 (“Sale Consideration”) (“Proposed Divestment”).

Further details are in the file attached.

This announcement is dated 5 February 2016. |

http://www.bursamalaysia.com/market/listed-companies/company-announcements/4996781

|

|

|

|

|

|

|

|

|

|

|

|

发表于 11-2-2016 01:45 AM

|

显示全部楼层

本帖最后由 icy97 于 11-2-2016 06:55 PM 编辑

脱售Optimax 美德再也专注建筑业

财经 2016年02月10日

美德再也(MITRA,9571,主板建筑股)以510万令吉脱售Optimax眼疗专科中心51%股权的计划,受到肯纳格研究分析员看好,並相信此举可使该公司更专注于旗下建筑业务。

美德再也上週五(5日)宣佈以510万令吉脱售Optimax眼疗专科中心的51%股权。

脱售活动预计將在2016年次季完成,而所得资金將作为营运资金以及偿还债务。

对此,分析员表示並不感到意外,因为该公司管理层早在去年4月份已有此念头。

「我们看好美德再也此次举措,相信可让该公司更专注于其核心业务。」

Optimax向来是该公司的非核心业务,对其2015財政年净利贡献预计仅有1.1%。分析员说,这次的脱售计划將为其2016財政年带来149万令吉的收益。

「在完成脱售后,我们预计美德再也的凈负债率,將由去年首9个月的0.29倍下滑至0.28倍。」

虽然该数额仍高于业內平均的0.22倍,但仍然处于舒適水平。

年头至今,美德再也仍未收穫任何合约,而该公司设下10亿令吉的订单目標。不过,该公司目前拥有14亿8000万令吉的订单,可保障未来2年的能见度。

另一方面,该公司的房產业务主要由旗下Wangsa9,以及即將推出的蒲种柏利玛(Puchong Prima)项目所带动,两者的发展总值分別为6亿8000万令吉,以及15亿令吉。

维持投资评级

「虽然房產领域放缓,但我们认为这对美德再也带来的影响有限。两个项目皆有卖点,与轻快铁(LRT)毗邻是其有利的地理优势。」

在扣除了Optimax的盈利贡献后,分析员將该公司2016財政年的核心净利预测下调1.3%至9780万令吉。

虽然如此,由于脱售资產后將得到一次性收益,因此分析员维持美德再也同期的净利预测。

在完成脱售后,分析员维持该股「超越大市」的投资评级,以及目標价1.63令吉。【东方网财经】

美得再也 售Optimax估值合理

财经 股市 行家论股 2016-02-11 11:56

http://www.nanyang.com/node/747628?tid=462

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-2-2016 05:56 PM

|

显示全部楼层

本帖最后由 icy97 于 25-2-2016 06:04 PM 编辑

美得再也获1.6亿合约

财经新闻 财经 2016-02-25 14:35

http://www.nanyang.com/node/749742?tid=462

(吉隆坡24日讯)美得再也(MITRA,9571,主板建筑股)获颁建筑合约,总值1亿5731万8909令吉。

根据文告,这项合约是由Putrajaya Homes,颁给Pembinaan Mitrajaya,后者将负责建筑及完成布城两栋一马公务员房屋计划(PPA1M),共800个单位。

合约为期36个月,预计可在2019年2月22日竣工,料能贡献未来净利。

| Type | Announcement | | Subject | OTHERS

| | Description | Mitrajaya Holdings Berhad ("MHB" or the "Company")Pembinaan Mitrajaya Sdn Bhd awarded contract for the proposed construction and completion of 800 units public apartments "Perumahan Penjawat Awam 1 Malaysia" inclusive of 2 blocks multi-level car park and common facilities at parcel 17RM2, Precint 17, Putrajaya | The Board of Directors of Mitrajaya Holdings Berhad (“MHB” or the “Company”) is pleased to announce that its wholly owned subsidiary, Pembinaan Mitrajaya Sdn Bhd has on 22 February 2016 accepted from Putrajaya Homes Sdn Bhd the award for the proposed construction and completion of 800 units public apartment “Perumahan Penjawat Awam 1 Malaysia” inclusive of 2 blocks multi-level car park and common facilities at parcel 17RM2, Precint 17, Putrajaya for a contract sum of RM157,318,909 only (“the Contract”).

The Contract is for duration of 36 months and is expected to be completed by 22 February 2019.

The Contract is expected to contribute positively to MHB Group’s future earnings.

None of the Directors or major shareholders of the Company and persons connected with such Directors or major shareholders have any interest in the Contract.

This announcement is dated 23 February 2016

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-2-2016 09:37 PM

|

显示全部楼层

本帖最后由 icy97 于 17-3-2016 01:54 AM 编辑

毛利突破1亿 美德再也财报亮丽

经济新闻

16/03/201619:08

http://www.kwongwah.com.my/?p=109599

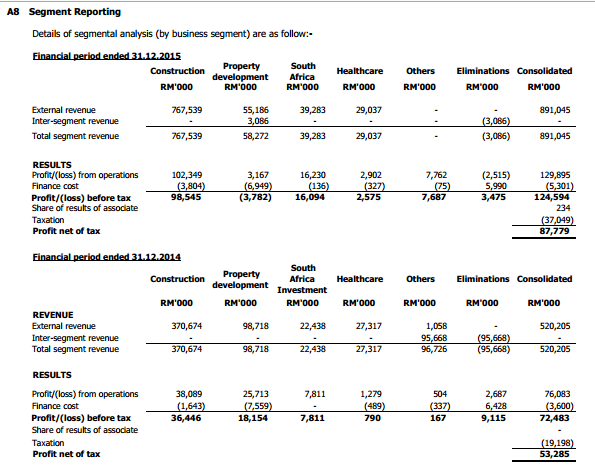

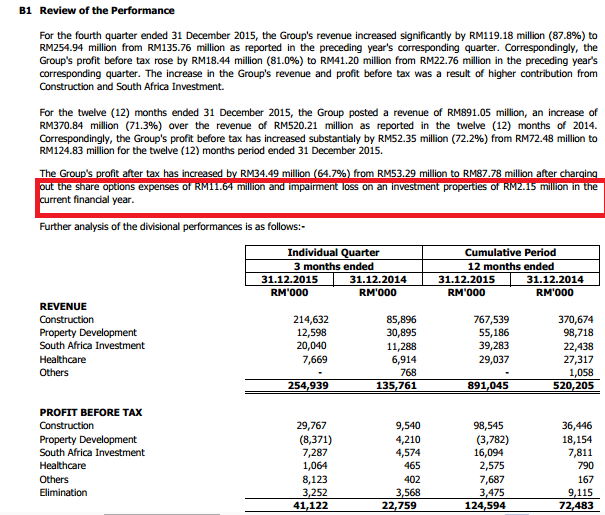

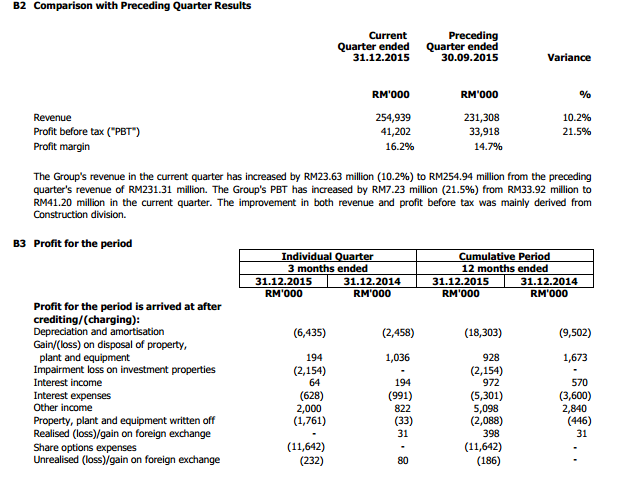

(吉隆坡16日讯)美德再也控股有限公司(MITRA,9571,建筑组)公布,在截至2015年12月31日止财政年,所取得的税前利润按年从7240万令吉上升至1亿2480万令吉。

该建筑集团致函大马交易所指出,至于营业额也由之前的5亿2000万令吉跳升至8亿9100万令吉。

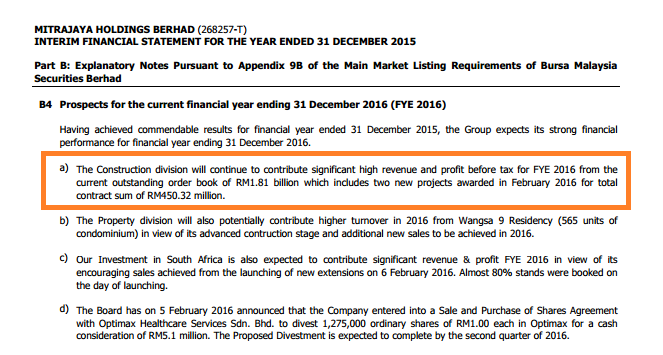

展望未来,它预计现财政年将会录得强劲的表现,主要是建筑业务继续贡献集团较高的收入和税前利润,而且目前手握总值18亿1000万令吉的订单合约。

美德再也在今年2月荣获两项总值4亿5032万令吉的新项目。

该集团表示,产业业务也将在2016年,通过Wangsa 9 Residency贡献较高的营业额。此外,在南非的投资,预计今年将会显著贡献集团的收入和利润。

| 9571 | | Quarterly rpt on consolidated results for the financial period ended 31/12/2015 | | Quarter: | 4th Quarter | | Financial Year End: | 31/12/2015 | | Report Status: | Unaudited | | Submitted By: |

|

|

| Current Year Quarter | Preceding Year Corresponding Quarter | Current Year to Date | Preceding Year Corresponding Period |

| 31/12/2015 | 31/12/2014 | 31/12/2015 | 31/12/2014 |

| RM '000 | RM '000 | RM '000 | RM '000 | | 1 | Revenue | 254,939 | 135,761 | 891,045 | 520,205 | | 2 | Profit/Loss Before Tax | 41,202 | 22,759 | 124,828 | 72,483 | | 3 | Profit/Loss After Tax and Minority Interest | 25,349 | 16,144 | 87,658 | 53,769 | | 4 | Net Profit/Loss For The Period | 25,323 | 16,089 | 87,779 | 53,285 | | 5 | Basic Earnings/Loss Per Shares (sen) | 3.95 | 2.73 | 14.03 | 9.10 | | 6 | Dividend Per Share (sen) | 5.00 | 5.00 | 5.00 | 5.00 |

|

|

| As At End of Current Quarter | As At Preceding Financial Year End | | 7 | Net Assets Per Share (RM) |

|

| 0.7800 | 0.9900 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-2-2016 09:38 PM

|

显示全部楼层

本帖最后由 icy97 于 25-2-2016 10:18 PM 编辑

【美德十二连霸】- MITRA(9571) 盈利yoy进步57%,2016年豪取4亿5000万建筑合约!

Thursday, February 25, 2016

http://harryteo.blogspot.my/2016/02/1123-mitra9571-yoy57201645000.html

今天笔者非常看好的建筑股MITRA的业绩终于出炉了,2015年的业绩以及盈利相比2014年分别上涨了71%以及63%。今年建筑领域的表现不俗,而MITRA的PE现在更是处在8.42的价格。除此之外,公司更是公布了5仙的股息,以现在RM1.15的股价计算,周息率大约是4.35%。这在建筑领域是非常出色的,所以MITRAJAYA在2016年应该会有不错的表现。

上图我们可以看到MITRA的盈利已经yoy连续进步12个季度了,这在马股里算是非常少见的。而Profit Margin从10.3%小跌到现在的9.8%,主要原因是产业部门的表现放缓。

上图是MITRA各大Segment在14以及15年的数据,大家可以看到MITRA建筑的税前盈利从36.446mil进步到15年的98.545mil。不过产业却从盈利18.154mil变成了亏损3.782mil。虽然产业放缓,但是建筑以及南非投资表现出色,弥补了产业的损失。全年税后的盈利增长到87.779mil,明年有望突破1亿马币。

其实这个季度的税前盈利是41.122 mil,不过因为11.64mil的share option exercise以及产业投资的2.15 mil拉低了盈利。

以上是include进profit的事项,Share Option expense就足足11.642 mil,不然这个季度Mitra是有机会突破历史新高的盈利的。

让人欣慰的是,MITRA在两天内公布了1.57亿以及2.93亿的合约,所以2016年2个月就豪取4.5亿合约,现在总合约是18.1亿。MITRA在2015年的营业额是8.91亿,手上的合约就够它们忙到2017年年底。

此外,公司在2月5号公布卖出Optimax Healthcare的股份,预计16年会有5.1 mil进账。而且预计16年产业segment会有所改进,所以有机会开始贡献盈利。而且公司今年预计还会陆续获得建筑合约,因此前景非常看好。

以上纯属功课分享,买卖前请做好功课。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-2-2016 04:35 AM

|

显示全部楼层

本帖最后由 icy97 于 29-2-2016 01:51 AM 编辑

美德再也獲2.9億工程

2016-02-27 16:52

吉隆坡27日訊)美德再也(MITRA,9571,主板建筑組)獲PJ Midtown發展有限公司頒發總值2億9千300萬令吉綜合產業建築以及外部工程。該公司在文告中表示,該項工程位於八打靈再也13區,將在2015年4月動工,為期26個月。(星洲日報/財經)

Type | Announcement | Subject | OTHERS | Description | Mitrajaya Holdings Berhad ("MHB" or the "Company")Pembinaan Mitrajaya Sdn Bhd awarded a mixed development Complex building and external works valued at RM293 million for PJ Midtown Development Sdn Bhd | The Board of Directors of Mitrajaya Holdings Berhad (“MHB” or the “Company”) is pleased to announce that its wholly owned subsidiary, Pembinaan Mitrajaya Sdn Bhd has on 25 February 2016 accepted from PJ Midtown Development Sdn Bhd the award contract for a mixed development Complex building and external works at Section 13 Petaling Jaya for a contract sum of RM292,999,999 only (“the Contract”).

The Contract will commence on 1 April 2016 for duration of 26 months and is expected to be completed by 31 May 2018.

The Contract is expected to contribute positively to MHB Group’s future earnings.

None of the Directors or major shareholders of the Company and persons connected with such Directors or major shareholders have any interest in the Contract.

This announcement is dated 25 February 2016. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 12-3-2016 01:02 AM

|

显示全部楼层

今天股价有点动静,可是找不到相关新闻?

1.18 +0.05 (4.42%)

|

|

|

|

|

|

|

|

|

|

|

|

发表于 18-3-2016 11:43 PM

|

显示全部楼层

本帖最后由 icy97 于 18-3-2016 11:46 PM 编辑

MITRA (Not Rated). Recently, small cap construction companies garnered investors’ interest after displaying stronger earnings performances as well as the surprise RM1.46b Pan Borneo highway contract win by KIMLUN and ZECON last Wednesday. MITRA has since been under investors’ radar as it rose 7.0 sen (5.93%) to close at RM1.25 on the back of strong trading volume. From a technical standpoint, the share price has staged a technical breakout from its resistance-turned-support level of RM1.22. MACD has conducted a bullish crossover to indicate a bullish outlook forward. This is supported by the rising buying momentum signalled by the upticks in the RSI and Stochastic. Should follow-through buying interest persist riding on the hype surrounding small cap construction players, we view that the share price could look to retest its immediate resistance level of RM1.30 (R1) soon before trending towards RM1.45 (R2) next in the near-term. Immediate support levels, on the other hand, are seen at RM1.22 (S1) followed by RM1.13 (S2).

Source: Kenanga Research - 15 Mar 2016

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-4-2016 09:53 PM

|

显示全部楼层

本帖最后由 icy97 于 10-4-2016 10:10 PM 编辑

【美德再也】-浅谈MITRA(9571), 2016年手握18亿1000万合约,2016年剑指10亿Market Cap!

Sunday, April 10, 2016

http://harryteo.blogspot.my/2016/04/1137-mitra9571-2016181000201610market.html

今年是建筑大年,很多大型的建筑合约都会在今年颁发。以股价涨幅来看,今年涨幅比较受人瞩目的就有KIMLUN, SUNCON, MUDAJAYA, TRC以及ARZB等公司。以上的公司的涨幅接近20%,相信今年的建筑合约还是陆续有来。

不过我今天要跟大家分享的就是MITRA - 美德再也这家市值808 mil的建筑股。而在马来西亚45家建筑股当中,MITRA的市值暂时排名第9。Mitra现在的PE是9.22,今年只要股价可以有25%的涨幅,Market cap就可以剑指10亿,摇身变成一家中型建筑股。以下是笔者对Mitra的一些帮助,希望可以对读者们有帮助。

- MITRA的盈利一直很稳定在成长, 上个季度的盈利更是突破新高。而这个季度因为ESOS花费了11.642 mil而导致盈利小幅度下跌。

- 如果把MITRA的业务分拆来看,建筑领域贡献了超过80%的盈利。而南非投资的盈利也越来越高,公司也在季度报告里说未来的盈利贡献会更加好。

- 不过美中不足的是,产业领域的盈利连跌了5个季度,这是可以预见的。幸亏南非投资的盈利弥补了产业领域的低迷。

- 而公司也表明已经售出了Healthcare的生意,相信在接下来的季度会收到一笔3 - 5mil的现金。

- 再看看Mitra的Profit margin, Q4一路以来是最强的季度。大家可以看到Q1 - Q3的PM都很稳健地上涨着, 第4个季度因为被产业部门拖累而导致Profit margin有所下跌。

- 但是仔细一看, MITRA在Q4的Profit BEFORE TAX 竟然有41.222mil, 这也是公司的新高。只是在Tax那里给了足足15 mil, profit after tax 就缩水了,主要是因为Share option expense is not tax deductible。

- 不过公司现在手握1,810 mil的合约, 可以继续忙碌到2017年。而且相信接下来LRT 3有可能会竞标到建筑合约, 今年的合约还是会陆续有来。

- MITRA最近季度的现金保持在31 mil左右, 2015年都保持在31 - 37 mil左右。

- 而TOTAL ASSET从2014年的634 mi进步到最新的1,018 mil.

- 不过,债务也有了“飞跃性”的进步,从2014年的98.04 mil上涨到现在的168.942mil。一年内债务上涨了70.81%,让笔者看了有点担心。

- 但是把债务和营业额比较,营业额也上涨了71.29%,所以理论上还是可以接受的。因为建筑领域的债务相对其他领域都会比较高的,只是希望在2016年现金流可以有所改善。

以技术图表来看,MITRA已经数次冲击1.28这个强力阻碍点。大家仔细看的话,不难发现3月的成交量有很大的提升。加上不少建筑合约即将出炉,希望MITRA可以分到一点猪肉,这样就可以在利空消息的刺激下突破RM1.30.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 16-4-2016 10:03 PM

|

显示全部楼层

建築業向好‧美德再也競標27億工程

2016-04-16 11:40

(吉隆坡15日訊)美德再也(MITRA,9571,主板建筑組)積極競標27億令吉新建築工程,以填補將在2年內干枯的訂單,分析員相信可負擔房產、輕快鐵、捷運和泛婆羅洲大道將是未來潛在合約更新主要來源。

MIDF研究表示,美德再也現持有18億令吉訂單,並競標27億令吉新工程,其中22億令吉來自建築工程,但泛婆羅洲大道並不包括在內。

以之前兩個配套合約價值來看,MIDF研究預計未來每個配套工程價值介於12億至18億令吉,若美德再也財團成功獲取其中一個工程,以30%持股來算,有望在未來4年帶來年均9千萬令吉營業額。

此外,南非投資也開始帶來回酬,該行預測南非業務貢獻將與2015財政年3千928萬令吉營業額及1千609萬令吉稅前淨利相符。

“鑑於過去幾年稅前盈利賺益穩定,加上建築業前景向好,我們給予該股1令吉56仙目標價。”( 星洲日報/財經) |

|

|

|

|

|

|

|

|

|

|

|

发表于 18-4-2016 11:44 PM

|

显示全部楼层

Date | Open Price | Target Price | Upside/Downside | Price Call | Source | News | 01/04/2016 | 1.24 | 1.77 | +0.53 (42.74%) | BUY | KENANGA | | 26/02/2016 | 1.17 | 1.77 | +0.60 (51.28%) | BUY | KENANGA | | 24/02/2016 | 1.17 | 1.63 | +0.46 (39.32%) | BUY | KENANGA | | 24/02/2016 | 1.17 | 1.95 | +0.78 (66.67%) | BUY | HLG | | 10/02/2016 | 1.09 | 1.75 | +0.66 (60.55%) | BUY | Malacca Securities | | 10/02/2016 | 1.09 | 1.63 | +0.54 (49.54%) | BUY | KENANGA | | 10/02/2016 | 1.09 | 1.95 | +0.86 (78.90%) | BUY | HLG | | 14/01/2016 | 1.17 | 1.95 | +0.78 (66.67%) | BUY | HLG | | 08/01/2016 | 1.19 | 1.52 | +0.33 (27.73%) | BUY | HLG | | 08/12/2015 | 1.21 | 1.95 | +0.74 (61.16%) | BUY | HLG | | 26/11/2015 | 1.28 | 1.63 | +0.35 (27.34%) | BUY | KENANGA | | 26/11/2015 | 1.28 | 1.95 | +0.67 (52.34%) | BUY | HLG | | 29/10/2015 | 1.21 | 1.63 | +0.42 (34.71%) | BUY | KENANGA | | 27/10/2015 | 1.21 | 1.63 | +0.42 (34.71%) | BUY | KENANGA | |

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3339

3339  61

61