|

|

发表于 28-2-2017 12:51 PM

|

显示全部楼层

发表于 28-2-2017 12:51 PM

|

显示全部楼层

本帖最后由 icy97 于 2-3-2017 06:47 AM 编辑

末季亏损引卖压 捷硕基本面仍强

财经 2017年02月28日

http://www.orientaldaily.com.my/business/cj200018300

(吉隆坡28日讯)儘管捷硕(JAKS,4723,主板建筑股)末季(截至去年12月31日止)业绩由盈转亏,而且全年净利急挫98%,导致该股今日因沉重卖压而大热下跌15仙或12.20%,至1.08令吉;惟,分析员认为,捷硕的基本面依旧强稳,並重申对该股「买进」投资评级。

捷硕去年末季净亏2403万令吉,前期则净赚2922万令吉;同时,该公司2016全年净利锐减98%,至74万令吉,前期为4147万令吉。

未纳入越南营收贡献分析员说,捷硕末季业绩不符预期,主要是没能將越南发电厂工程、採购及建造(EPC)合约的营业额贡献纳入计算,同时也承担一次性的拨备开销。

大眾投行分析员表示,该公司在去年已认列越南发电厂设备製造业务的部份营业额,惟末季时却被迫只能在设备製造完成並交付后,才能认列这笔营业额。

「在缺乏越南的营业额贡献,捷硕末季只靠本地的建筑工程来推动营业额成长。该公司目前在本地的订单额预计为27亿6000万令吉,而越南的发电厂工程大约是27亿4000万令吉。我们预计越南工程將会在下半年开始做出贡献。」

该公司的太平星(PACIFICSTAR)產业发展项目在末季贡献良多,未入账销售高达3亿6160万令吉。

惟,分析员说,该公司產业业务依然受EVOLVECONCEPT商场的730万令吉亏损拖累,捷硕持有该商场51%的股权,或相等于须承担370万令吉亏损。

分析员指出,捷硕在末季为MENARASTAR2做了1100万令吉的工程延误赔偿(LAD)拨备,但分析员相信该公司能够收回这笔拨备。

另外,艾芬黄氏分析员也称,由于令吉在去年急贬,拖累捷硕去年在越南的投资,令该公司去年的外匯亏损达820万令吉。

「不过,越南的联营公司隨后已退还这笔亏损,而我们也將这笔外匯亏损看作一次性项目。」

大眾投行与艾芬黄氏投行均给予该股「买进」投资评级,並分別將目標价设在1.50令吉和1.70令吉。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 5-3-2017 06:26 AM

|

显示全部楼层

发表于 5-3-2017 06:26 AM

|

显示全部楼层

Type | Announcement | Subject | NEW ISSUE OF SECURITIES (CHAPTER 6 OF LISTING REQUIREMENTS)

FUND RAISING | Description | JAKS RESOURCES BERHAD (JRB OR THE COMPANY)PROPOSED PRIVATE PLACEMENT OF UP TO 43,836,100 NEW ORDINARY SHARES OF JRB REPRESENTING APPROXIMATELY 10% OF THE EXISTING TOTAL NUMBER OF ISSUED SHARES OF JRB ("PROPOSED PRIVATE PLACEMENT") | On behalf of the Board of Directors of JRB (“Board”), Kenanga Investment Bank Berhad (“Kenanga IB”) is pleased to announce that the Company proposes to undertake the Proposed Private Placement.

Please refer to the attachment for further details.

This announcement is dated 27 February 2017. |

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5350389

|

|

|

|

|

|

|

|

|

|

|

|

发表于 6-3-2017 07:02 PM

|

显示全部楼层

本帖最后由 icy97 于 6-3-2017 10:31 PM 编辑

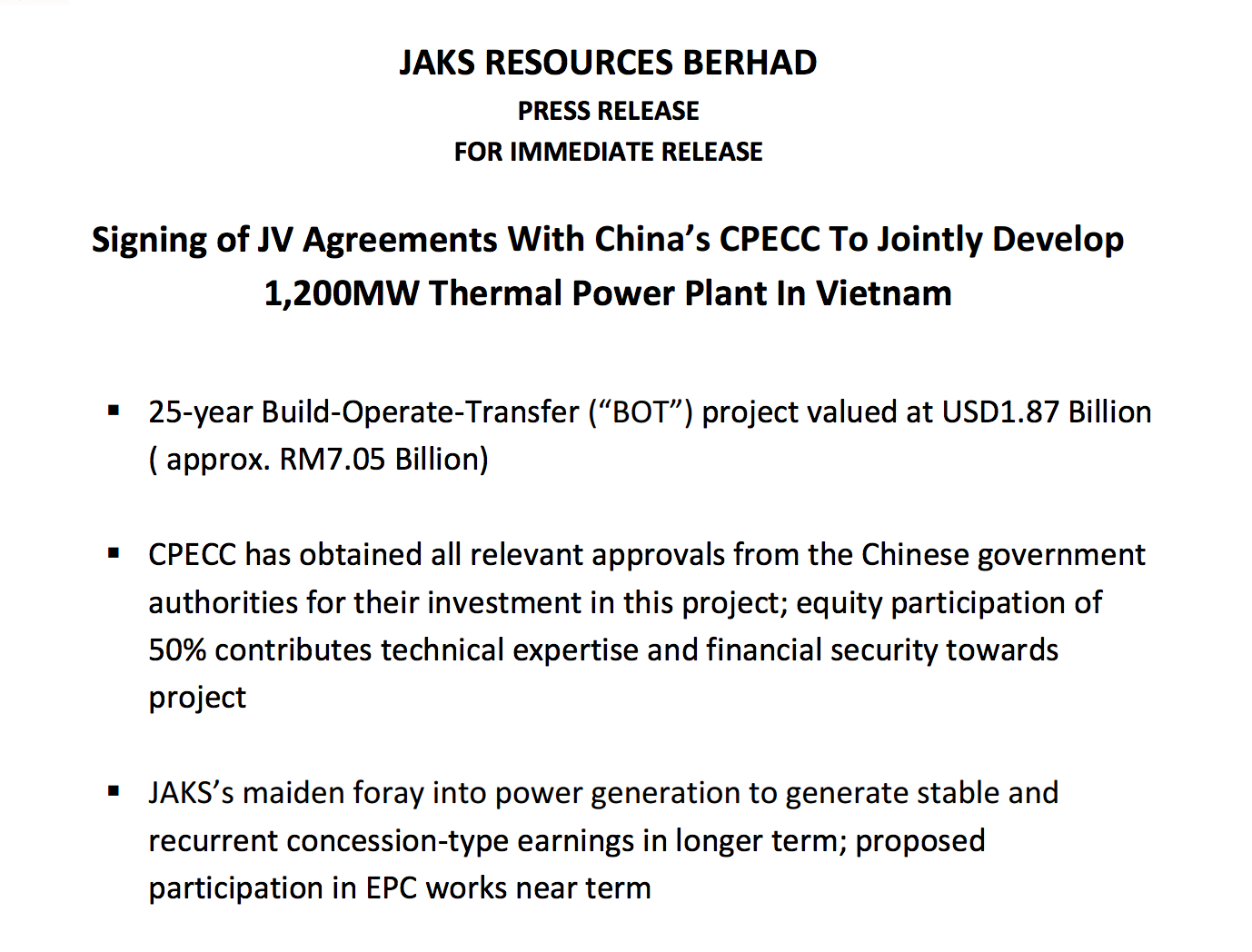

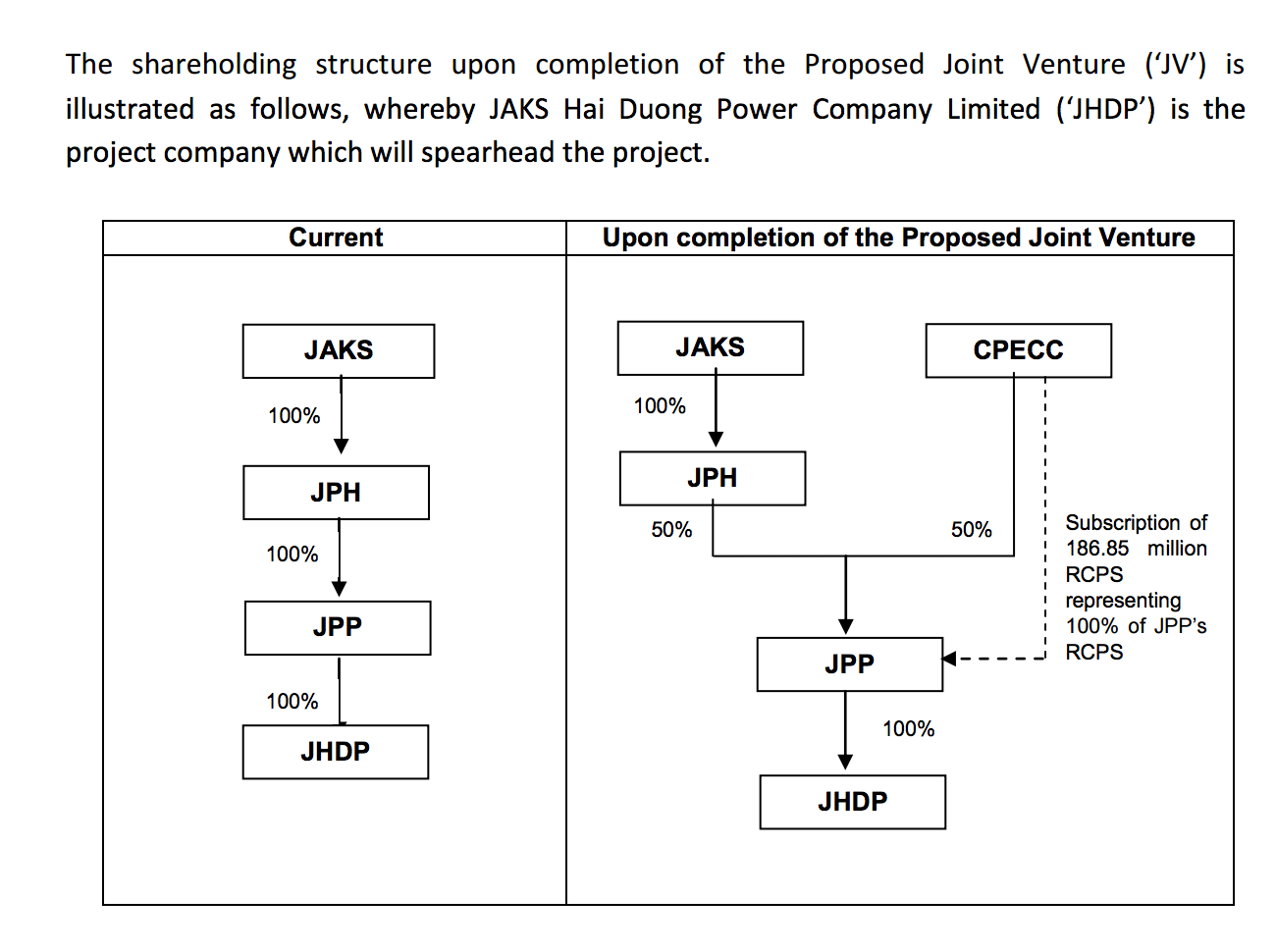

JAKS: Great idea but is it great execution?

Saturday, March 4, 2017

http://www.intellecpoint.com/2017/03/jaks-great-idea-but-is-it-great.html

I have to give it to Mr Koon. He sees a good company with a very good project. Basically, Jaks Resources without the power plant project is an average company but with the IPP project it is a more than an average company with an attractive price.

What has it gotten with the PPA in Vietnam? Basicially as below, a BOT (transfer - after 25 years) project and its partner CPECC has bought into the project by funding a huge portion of it.

What JAKS has to do now (which it has done) is to fulfill its portion by coming out with USD140.14 million while CPECC will come out with the other portion. In addition, CPECC will build the bulk of the project and come out with Redeemable Convertible Preference Shares (RCPS) to fulfill the equity portion. (On top of that, the RCPS comes with zero dividend costs) CPECC has also gotten the financing for the project as well with its corporate guarantee. It should be noted that CPECC is huge power plant consulting company in China. Its parent, China Energy Engineering is a HKD43B company, which means and says a lot.

The structure is as per below:

Ultimately, JAKS can own up to 40% of the project and it now has a partner whom can deliver. On top of that, it gets a substantial portion of work which can be translated into construction profits from this project.

Do I have reason to believe it can be delivered? Yes.

Do I have reason to trust the project has decent to good return? I should think so considering the interest from CPECC. It has country risks obviously, but this one sounds to be more secure.

Now, all that is good as if it is able to secure good IRR, this basically is a great investment with Jaks trading at about RM535 million valuation. (Jaks has mentioned of it eyeing at least a 10% IRR.)

With that, it is definitely not wrong for a person who understands construction to wallop - and wallop he did. Another point to note is that the controlling shareholder - Mr Ang Lam Poah only owns around 8% to 9% of the company on paper. (I would tend to think he definitely has supports from his other friendly shareholders.) What Mr Ang did wrong was that he took a long time to accumulate the shares, probably thinking of getting them at cheap - below RM1.

Seeing opportunities (probably), Mr Koon Yew Yin bought the shares in a very quick manner and in the process, accumulated more than 11% over a short period of time. (Mr Koon is now, the single largest shareholder) At the point of him becoming a substantial shareholder, it triggered the attention of Ang's group, I believe. Jaks announced an unusual quarterly 31 Dec 2016 loss and at the same time, announced that it is to do a 10% private placement.

| KYY's holding has increased to 11.7% by 1 March 2017 |

Does Jaks has enough bullets to defend the onslaught? I should think so. It has many defensive tools to do that - and it has already done so by announcing a private placements. Private placements as we know can go to friendly parties. Basically, Jaks can do many more of private placements and as long as Koon does not acquire enough to take control - he can't do much. (That has been proven in the case where QL was unable to takeover Lay Hong, and QL I would think is even deeper pockets, but they can't do much.)

Can Mr Koon do much? We shall see. And I do not think he is keen to takeover anyway - as the project is for Mr Ang to lose (he is the person, whom have worked hard to pull everything together), moreover Koon is not in the right age to do that. A new management could jeopardize the project.

Mr Koon's past records have been more of a short to medium term investor - come in - make a kill and go. With that, (I would think) Mr Ang has reasons to be afraid and not to entertain much requests. The ball is in Ang's court to play and decide how to play.

(You see, if I have Warren Buffett as my shareholder, I should feel proud. But, if I have Carl Icahn as my shareholder - I would put on more defences surrounding me, because of animal instincts. In this case though, activists investing may not work well.)

Will someone like Mr Koon ask for a favourable return from the shares? Almost a surety. Why would he invests into Jaks anyway? - and this manner of buying.

The biggest question is - if Jaks current controlling shareholders do not want to play ball - the shares can be stuck at RM1.10 to RM1.30 for a long time - something that a shorter term shareholder would not want! It could end up being you buy to push up your own share price. You can buy but you cannot sell at a profit.

One thing for sure (unless with a deal being made, the private placements may not be that cheap - at least not the type of price which Ang and his group have been buying at i.e. around RM1 - and the way Mr Koon has been buying.)

This is quite interesting turns out and a lesson to note in the long term.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 9-3-2017 05:43 AM

|

显示全部楼层

Notice of Interest Sub. S-hldr (29A)Particulars of Substantial Securities HolderName | MADAM TAN KIT PHENG | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary Shares | Name & address of registered holder | HLIB NOMINEES (TEMPATAN) SDN BHDPLEDGED SECURITIES ACCOUNT FOR TAN KIT PHENG (M)MAYBANK NOMINEES (TEMPATAN) SDN BHDPLEDGED SECURITIES ACCOUNT FOR TAN KIT PHENGTA NOMINEES (TEMPATAN) SDN BHDPLEDGED SECURITIES ACCOUNT FOR TAN KIT PHENG |

| Date interest acquired & no of securities acquired | Currency | Malaysian Ringgit (MYR) | Date interest acquired | 06 Mar 2017 | No of securities | 22,369,700 | Circumstances by reason of which Securities Holder has interest | Acquisition | Nature of interest | Direct Interest | Price Transacted ($$) |

|

| | Total no of securities after change | Direct (units) | 22,369,700 | Direct (%) | 5.103 | Indirect/deemed interest (units) |

| | Indirect/deemed interest (%) |

| | Date of notice | 07 Mar 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-3-2017 04:09 AM

|

显示全部楼层

| 1. Details of Corporate Proposal | Involve issuance of new type/class of securities ? | No | Types of corporate proposal | Private Placement | Details of corporate proposal | PRIVATE PLACEMENT OF UP TO 43,836,100 NEW ORDINARY SHARES OF JRB REPRESENTING APPROXIMATELY 10% OF TOTAL NUMBER OF ISSUES SHARES OF JRB | No. of shares issued under this corporate proposal | 43,836,100 | Issue price per share ($$) | Malaysian Ringgit (MYR) 1.3600 | Par Value ($$) | Malaysian Ringgit (MYR) 0.000 | | Latest issued and paid up share capital after the above corporate proposal in the following | Units | 482,197,172 | Currency | Malaysian Ringgit (MYR) 0.000 | Listing Date | 24 Mar 2017 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 31-3-2017 11:57 PM

|

显示全部楼层

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

RELATED PARTY TRANSACTIONS | Description | JAKS RESOURCES BERHAD ("JRB" OR THE "COMPANY")INVESTMENT IN NEW SUBSIDIARY-Fortress Pavilion Sdn Bhd | The Board of Directors of JAKS Resources Berhad (“JRB” or the “Company”) wishes to announce that the Company’s wholly owned subsidiary, JAKS Sdn Bhd (“JSB”) has on 29 March 2017 acquired 51 ordinary shares, representing 51% equity interest of the enlarged paid-up capital in a new company, Fortress Pavilion Sdn Bhd (“FPSB”) at a cash consideration of RM51 (“the Investment”). The balance of 49% equity interest in FPSB is held by Island Circle Development (M) Sdn Bhd (“ICD”), a major shareholder of JRB’s 51%-owned subsidiary, JAKS Island Circle Sdn Bhd.

Further details are in the attached file.

This announcement is dated 30 March 2017. |

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5381117

|

|

|

|

|

|

|

|

|

|

|

|

发表于 28-4-2017 03:52 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 21-5-2017 02:38 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-5-2017 07:48 PM

|

显示全部楼层

本帖最后由 icy97 于 23-5-2017 01:02 AM 编辑

Is Jaks a big fat frog jumping all around? kcchongnz

Author: kcchongnz | Publish date: Mon, 22 May 2017, 01:29 AM

https://klse.i3investor.com/blogs/kcchongnz/123266.jsp

“Jaks has secured agreements which include a land-lease deal, a power plant agreement, build-operate-transfer (BOT) contract, coal-supply agreement and a government guarantee. More importantly, it has roped in an established power plant builder, China Power Engineering Consulting Group Co Ltd (CPECC) as its equity partner to build a 1200 MW coal-fired power plant in Hai Duong province, Vietnam. The JV company has also secured US$1.4bn (c.RM5.8bn) in financing, or 75% of project costs. Works have commenced in 2QCY16, with the first phase to be completed by 2020. We expect its near term earnings to be underpinned by its Vietnam engineering, procurement and construction (EPC) contract worth RM1.9bn.

Jaks, together with CPECC, is constructing a BOT power plant, with an estimated cost of US$1.87bn with 25 years’ concession and power purchase agreement with Viet Nam Electricity (EVN). US$1.4bn already secured back in September 2015 from Industrial and Commercial Bank of China, China Construction Bank Corporation and Export-Import Bank of China. The JV has US$160m capital (equity portion) and expects the remaining balance of US$307.1m to be injected in the next 3 years. Management expects strong IRR in the mid-teens with the first unit expected to be completed by mid-2020, and the second unit 6 months later.”

Source Public Investment Bank Berhad, January 10 2017.

The JV for the power plant development requires capital to develop this project, in return, they are rewarded with regular income from the sale of electric power over a period of 25 years, at a rate of return, I term it as an Internal rate of return, IRR.

How good is this project? We will have to do a financial analysis of the project based on the net present value (NPV), or internal rate of return (IRR) using the cash inflows and outflows from the project. This we need some knowledge of finance.

The link below explains what NPV and IRR are and their importance in assessing the viability of a project.

http://www.investopedia.com/walk ... r/introduction.aspx

According to the report from Public Investment Bank, the cost of the power plant development is estimated to be USD1.87 billion. 75% of the cost, or USD1.4 billion has been secured. The equity portion of the joint venture, JV, is 30%, or USD470 million, of which USD160m had been paid up, with the rest of USD310m, or RM960m, to be injected in the next three years. Part of the additional equity injection will be from the construction “profit” of about RM400m, or estimated 20% profit from the RM1.9b EPC works.

The construction “profit” is just an accounting number, from left pocket to right pocket, and back to left pocket, assuming each partner has the same share of the cake of 70-30 as the JV partnership. In fact, the JV has to find another RM560m from somewhere to be injected into the JV as equity.

As you can see, there are cash inflows and outflows to and from Jaks and CPECC; inflows such as construction profits, regular income from power sales, outflows such as equity injections, initial as well as for the next few years.

All the numbers above may not be correct, as I have to admit that I do not know much about this project, but merely share the little that I know and what I thought. The pertinent questions are; what is the NPV, and what is your required return?

For NPV computations, we need to estimate all these future cash outflows and inflows at different periods, and discount them back to the present with a discount rate. The discount rate will depend on many factors, some of which are as below:

- Inflation rate

- Currency risk

- Risk free rate

- Execution risk

- Construction risk

- Coal supply risk

- Partnership risk

- Payment risk

- Political risk

- Social and environmental risk

- Others

Currently the 10-year government bond rate is 5.8%, and inflation rate is about 4.5%. The Vietnamese Dong was known to be volatile historically.

What would be your required return if you were to invest in a business in Vietnam with all the risks above?

For me, my required return will be a summation of risk free rate plus a risk premium. The risk premium will depend on how risky the project is, and how uncertain are the future cash flows estimations. For a normal business locally, my required return would be around 10%-15%.

If your required return is say 6%, lower than the estimate IRR of “mid-teens” as given by the Public Investment Bank report, you would probably be safe and would get a high positive NPV, which is good. Otherwise your NPV will be negative, a project which should never be started. This is because capital is a scarce resource. There is opportunity cost, and there are risks.

If your required return is substantially lower than the estimated IRR, you probably will be ok investing in Jaks. However, if your required return is substantially higher than the estimated IRR, you would be in for financial trouble.

Hence, the viability of investing in Jaks solely depend on your required return compared to NPV or IRR and the accuracy of estimation of future cash flows. The construction “profit” is just a smokescreen, unless Jaks is the contractor doing most of the EPC works and reward itself, itself only, with big fat construction margins.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-5-2017 02:39 AM

|

显示全部楼层

本帖最后由 icy97 于 3-6-2017 05:37 AM 编辑

越南合约上轨.捷硕首季净利翻6倍

(吉隆坡24日讯)在越南独立发电厂工程、采购和建筑(EPC)合约扶持下,捷硕(JAKS,4723,主板建筑组)截至2017年3月31日第一季净利翻了6倍,从前期的107万1000令吉暴增至754万4000令吉。

首季营业额为1亿5478万8000令吉,比去年同期的1亿2280万7000令吉增长26.04%。

该公司首席执行员洪南坡在文告中表示,在强稳合约扶持下,乐观相信集团表现将令人满意,其中总值4亿5450万美元的越南独立发电厂EPC合约上轨,预期相关建设工作将为集团未来数年盈利作出显著贡献。

“我们将继续在国内和越南竞逐多元道路、水务、电力和排污基础建设合约,以扩大建筑合约总量。目前,捷硕手握26亿令吉建筑合约,其中越南独立发电厂为期25年的EPC合约占18亿9000万令吉,而新街场—淡江高架大道(SUKE)贡献5亿零850万令吉;产业发展臂膀未入账销售则为1亿9760万令吉。”

越南发电厂EPC贡献6230万

回顾首季,捷硕建筑臂膀营业额增长51%至1亿2020万令吉,归功于越南独立发电厂EPC带来6230万令吉贡献,连带推动税前盈利走扬至1550万令吉,其中越南独立发电厂EPC建设即占1490万令吉。

受产业市场低迷影响,产业发展臂膀营业额下跌11.62%至3270万令吉,而Evolve概念广场的高营运、融资和折旧费用,以及清算及确定赔偿等因素拖累,导致产业发展业务亏损扩大,从前期的350万令吉增至1000万令吉。

文章来源:

星洲日报‧财经‧2017.05.24

SUMMARY OF KEY FINANCIAL INFORMATION

31 Mar 2017 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 31 Mar 2017 | 31 Mar 2016 | 31 Mar 2017 | 31 Mar 2016 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 154,788 | 122,807 | 154,788 | 122,807 | | 2 | Profit/(loss) before tax | 2,958 | 242 | 2,958 | 242 | | 3 | Profit/(loss) for the period | 2,622 | -1,178 | 2,622 | -1,178 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 7,544 | 1,071 | 7,544 | 1,071 | | 5 | Basic earnings/(loss) per share (Subunit) | 1.72 | 0.24 | 1.72 | 0.24 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 1.1900 | 1.1500

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 5-6-2017 09:54 PM

|

显示全部楼层

本帖最后由 icy97 于 5-6-2017 11:49 PM 编辑

Investors Should Look at the Company's Business - Koon Yew Yin

Author: Koon Yew Yin | Publish date: Sat, 3 Jun 2017, 09:26 PM

https://klse.i3investor.com/blogs/koonyewyinblog/124591.jsp

Most investors are short term traders. They look at the quarterly announcements and the price charts but they do not examine what kind of business the company is doing.

For example, when JAKS reported losses in its annual accounts, most of the short term investors just dumped their holdings as if there was no tomorrow.

If you look at JAKS’ announcement on 28th February of its losses, you can see that I bought 6.9 million shares at Rm 1.06 per share. Since then my wife and I have accumulated a total of 138 million shares and became the controlling shareholders.

We bought so much shares because JAKS has secured the contract to build 2 X 600 MW coal fired power plant for Rm 7.6 billion to sell electricity to the Vietnamese Government for 25 years. JAKS has subcontracted the whole project to the Chinese party which has been involved in 90 % of the production of electricity in China.

I know how much profit JAKS will make every year for 25 years as an Independent Power Producer (IPP).

When I was Managing Director of Mudajaya, we built almost all the 19 coal fired power plants in Malaysia as a contractor and not as the owner. As you know, contractors do not make much money. Owners of power plants make fantastic amount of money because they are selling electricity to consumers who have no alternative but to buy from them.

Most of the plants are currently owned by TNB, Tan Sri Syed Mokhtar and Tan Sri Yeoh Tiong Lay. According to the latest report of the top 50 richest men in Malaysia, Yeoh Tiong Lay is No 7 and Syed Mokhtar is NO 10.

As the controlling shareholder, I believe with my long experience in doing business, I can help JAKS to make more profit.

For a start, I will not want the company to tender any more construction contracts. Studies has shown that almost all construction contracts cannot be completed on time. The biggest obstacle that all contractors have to overcome is the open competitive tender system, the cheapest tender gets the contract.

In order to achieve the cheapest price, every tenderer has to be very optimistic while making his estimate. He has to assume that he can get all the required labour and materials at the current prices. He has also to assume that he will not meet inclement weather during construction.

When he is awarded the contract, almost all his assumptions will not come true. Due to inflation and many other reasons, the prices of labour and materials invariable are higher than what he has allowed in his tender. There is also more rain than he has assumed.

Moreover, he has construction difficulties which he did not foresee during tender preparation.

As a result, almost all construction contracts cannot be completed within scheduled time.

In fact, one of JAKS’ contracts is already being penalised for late completion.

After many decades of experience in the contracting industry, I have developed a system or method to complete contracts within programmed time to save cost and avoid penalty for late completion.

JAKS Must Concentrate on Producing Electricity Business

JAKS must concentrate in getting another contract to build coal fired power plant. As I said earlier, getting contract to build power plant to sell electricity is so profitable, I will help JAKS secure another contract in Myanmar. If you visit Yangon, you can see that almost every shop has a standby diesel power generator because there is a terrific shortage of electricity supply.

About 4 years ago, I arranged Mudajaya to sign a MOU with the Chief Minister of Mandalay to build a coal fired power plant in Mandalay which you can see the photo of the signing ceremony below.

Unfortunately, we could not find a consortium of banks to finance the project. Now with the Chinese partner, I believe I can arrange JAKS to undertake a contract to build a coal fired power plant in Myanmar.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 6-6-2017 09:48 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 23-6-2017 06:08 AM

|

显示全部楼层

本帖最后由 icy97 于 23-6-2017 06:21 AM 编辑

Jaks资源:产业子公司需“一段时日”方能转亏为盈

Adela Megan Willy/theedgemarkets.com

June 22, 2017 16:54 pm MYT

(吉隆坡22日讯)Jaks资源(Jaks Resources Bhd)在截至2016年12月31日止的财政年(2016财年)及2017年3月31日止的财年首季(2017财年首季)的盈利受蒙亏的产业部所冲击,并称产业部需一段时间才能转而获利。

Jaks资源企业策略总经理Elaine Tai表示,在产业市场极具挑战的情况下,该集团正“竭尽所能”引入合适的租户,以推动商场人流,尤其是坐落于八打灵再也Ara Damansara的Evolve Concept商场(Evolve Concept Mall)。

“Evolve Concept商场是在2015年杪开幕,因此,至今仍不足两年。一般来说,购物商场需要一段时间才能达到开始赚钱的一定阶段。此外,零售业面临供过于求的窘境。”

她是在Jaks资源今日的常年股东大会后,向记者如是指出。

“尽管如此,我们正尽力引进合适的租户来填满商场,以带动商场的人流。随着(Ara Damansara)轻快铁(LRT)站开通后,人们前往该商场也更为便捷,但我们也祭出更多方案来提高出租率。”

Tai表示,由于Evolve Concept商场的营运及融资费用较高,加上产业市场放缓,从而导致产业部蒙亏,这种情况料将“持续一段时日”,该集团希望未来几季的亏损将收窄。

Jaks资源企业策略高级总经理洪诗荣指出,该集团仍计划出售Evolve Concept商场,“倘若售价合适”,如今仍与有意收购的买家在洽谈中。

“像现在这样的市场情况是极为艰巨的,因为巴生谷地区的购物商场正蓬勃发展。我们的意图(出售该商场)一如既往...若售价合理的话。我们与有关方面的洽谈仍在进行中。”

“你可以质疑规划部分,但在8年前,当时巴生谷地区并没有许多购物商场。但是,突然之间,(许多其他的产业)公司开始推出相同的产品,从而导致零售产业过剩,犹如我们今日所看到的。”

该集团2016财年净亏1597万令吉,相比2015财年净赚4716万令吉;营业额也从2015财年的4亿6118万令吉,增加至2016财年的6亿4038万令吉。

Jaks资源2017财年首季净赚754万令吉,相比2016财年同季录得107万令吉。现财年首季营业额攀高至1亿5479万令吉,同期报1亿2281万令吉。

(编译:倪嫣鴽) |

|

|

|

|

|

|

|

|

|

|

|

发表于 23-6-2017 12:46 PM

|

显示全部楼层

本帖最后由 icy97 于 23-6-2017 08:30 PM 编辑

JAKS捷硕 - 第15届股东大会

昨天 (6/22) 是JAKS一年一度的股东大会,在旗下的【EVOLVE】商场举行。对于一家充满争议及讨论的公司,本专页当然不能错过。出席这次的大会的股东超过100名,其中持有集团约29%股权的官先生及妻子也高调出席,坐在台前的第一排。

目前,JAKS的大部分建筑工程的进度良好,其中一项已在完工阶段。至于发展总值高达USD454m (RM1.9b) 的越南发电厂,集团在近两年已经列认大约RM210m,剩余的RM1.7b将在未来三年逐步列认,而收入列认高峰期将落在2018-2019年。这发电厂工程的赚幅为20%,目前仍处于初步阶段,预计可在今年获得介于RM50-80m的盈利。这对于以往盈利缺乏稳定性的JAKS来说,是极为关键的收入。

然而,集团的业绩很大程度还需要取决于【EVOLVE】商场的表现。其产业发展部门在FY16蒙受RM36.7m的税前亏损。目前,管理层仍在寻找潜在买家,以脱售

【EVOLVE】商场。JAKS早前曾与一名新加坡的潜在买家处于脱售谈判的最后阶段,但是零售市场放缓导致这谈判最终被搁置。管理层表示当初决定建设【EVOLVE】商场,主要因为看中这地点靠近LRT以及高速公路。既然如今已经完成建设,惟有尽最大的努力把商场搞好。这一区域的商场不只是【EVOLVE】表现不好,其他如【CITTA】、【PARADIGM】和【EMPIRE】的表现也是如此。

在问答环节上,官先生首先表达他对JAKS今年的私下配售计划不满。当时市场的投资情绪高涨,为何集团还愿意以折价卖给第三者?管理层表示这批股权全卖给投资机构以及基金,主要利用5天市场平均价来计算出RM1.40的价格,再附上3%的折扣。

之后,官先生三番四次给予管理层忠告,表示他是IJM、GAMUDA以及MUDAJAYA的创办人,在建筑领域已有超过50年的经验。基本上,世界各地大部分的建筑项目都无法准时完工,全都需要延长时间完成。既然JAKS已有多项正在进行中的建筑项目,为何还要竞标那么多项目?倒不如把重心放在准时完工,提高建筑利润,以及清理全部不该有的赔偿和拨备 (Clean up all the shit) 。

JAKS在去年第4季度为PJ的【THE STAR】项目做了RM11m的工程延误赔偿 (Liquidated & Ascertained Damage) 拨备。这项目的发展总值为RM1b,原本预计在2016年杪完成。然而,由于工程出现了一些意外,这导致项目预期完工日期被逼延迟至2017年杪。管理层预计仍然还有RM15-20m的工程延误赔偿将被征收。奇怪的是,为何在场的股东们却没有任何反应?!

管理层针对官先生的看法作出了回应。JAKS早前有两项位于彭亨和沙捞越的项目都提早完工及交付。至于一些无法预期完成的项目,这主要因为政府在土地收购及赔偿方面多次展延,与JAKS的执行能力无关。政府也在之后批准JAKS把完工日期额外延迟380-400天。此外,政府已退还高达RM7m的工程延误赔偿给予JAKS,这将反映在下个季度业绩上。

最后,有股东提议让官先生进入董事局,毕竟官先生是经验老道的前辈,可以为管理层提供非常宝贵的建议。其实,身为单一大股东的官先生一直以来都有意愿进入董事局,早前更曾经为此事私底下发电邮给JAKS的常务董事MR. ANG,但是却得不到后者的回复。这也不难理解,毕竟MR.ANG最近频密从公开市场回购JAKS股票,相信是为了维护自己的权益。或许,管理层都无意让官先生进入董事局,以避免后者干涉集团业务上的决策。

官先生随后站出来,并霸气地说道:“没关系,我会通过特别股东大会 (EGM) 以及正确的手续和方式进入董事局,除非你们任何一个人可以购买比我更多的股权。我背后就有一班支持我的投资者。”最后,他也强调他已经80多岁了,不会以个人名义进入董事局,而是点名一位适合的人选担任这个岗位。JAKS的董事部有必要重新洗牌,把对集团业务没有贡献的董事踢出董事局。

结果,最后的决议 (Resolution) 投票结果显示,两项重新让董事进入董事局的决议遭到46%股东反对,股票数量高达129m。其他的决议都以99%股东赞成顺利通过。如没推断错误,拥有如此庞大股票的股东除了官先生及其妻子,别无他人。

整体来说,管理层展现出智慧的一面,一一回答股东们对于业务上的问题。然而,却有一名股东故意刁难管理层,所提出的不满都是专注在小细节上。他表示管理层给予的RM25食物现金券不足以替他消气,多番要求再额外给予更多的现金券。他也投诉商场的一些食物摊位在10点后仍未营业,导致一早赶来的他无法享有早餐。“When I am hungry, then I will be very angry”。管理层显得有些无奈,主席多次打断这名股东的对话,并表示请转移话题回到公司的业务上。

可以肯定的是,若官先生执意要进入董事局,相信这是无法避免的,毕竟在场的大部分股东都支持官先生。未来,管理层的一举一动肯定倍受瞩目,不容易当啊!

RH Research |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-6-2017 04:14 AM

|

显示全部楼层

捷硕可继续持有吗?

新山投资者xc问:

捷硕(JAKS,4723,主板建筑组)已经涨了一段时间,我算算大概赚了20%,请问还可以继续持有吗?股价还会继续涨吗?

答:事实上,自今年初以来,捷硕股价回酬率已达49%,分析员认为,该公司脱售资产进一步减轻净负债,是为下个催化因素,甚至可成为净现金公司,使它更有能力在国内外市场攫取更多工程合约。

捷硕有意售资产减债

肯纳格研究指出,捷硕管理层仍有意要脱售资产以进一步减轻公司的债务,包括脱售Evolve购物中心,以及其座落在首邦镇的一块占地15英亩的地皮,预料将可筹得4亿至5亿令吉资金,从而成为一家净现金公司。

该行预测其2017及2018财政年核心净利分别为4150万及5610万令吉,从2016财政年疲弱表现强力反弹,使其按年净利成长超越100%,主要由建筑业务推动,特别是尚余的国内外工程订单达26亿令吉支撑。

该行指出,捷硕在2016财政年时,其国内外建筑工程计划因各种因素而面对一些延迟问题,惟至2017年首季则出现显著回弹,使其建筑业务的营业额按年走高51%,其中60%为本地工程,其余40%则来自越南的工程。

未来2年盈利来自建筑业

预料未来2年的盈利将主要来自建筑业,特别是手握尚余工程订单达26亿令吉,其中63%来自越南,其余则是国内工程。

自该行于2016年3月推荐短线买进该公司股票,当时股价为1令吉53仙,该公司盈利表现走低,使2016财政年净利跌至70万令吉(2015年净利为4150万令吉),主要是投资的产业——Evolve概念购物中心出现不可预见亏损,以及勿述及太平洋之星工程计划蒙受损坏及清盘,惟今年首季开始,该股已经反弹回扬。

该行估计,该公司在综合价值估值下的合理价为1令吉54仙,并给予“套利”建议,因2018财政年预测本益比已达12.0倍水平,较同侪平均11.0倍还高,特别是过去曾经出现盈利波动的记录。

捷硕2016财政年的净负债率达到0.86倍高水平,管理层向来都在为旗下的Evolve购物中心寻找合适买家以减轻债务。该公司在2017财政年首季时的净负债率大幅度降低至0.63倍,主要是通过私下配售新股筹得5960万令吉的资金。

文章来源:

星洲日报‧投资致富‧投资问诊‧文:李文龙‧2017.06.28 |

|

|

|

|

|

|

|

|

|

|

|

发表于 21-7-2017 01:45 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 2-8-2017 01:52 AM

|

显示全部楼层

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

NON RELATED PARTY TRANSACTIONS | Description | JAKS RESOURCES BERHAD (JRB or the Company)Proposed Disposal of Property by Wholly-Owned Subsidiary, Premier Place Property Sdn Bhd | The Board of Directors of JRB wishes to inform that the Company’s wholly-owned subsidiary, Premier Place Property Sdn Bhd (“Premier Place”) has on 31 July 2017 entered into a Memorandum of Agreement (“MoA”) to dispose of the property owned by Premier Place at Subang Jaya, Selangor to Sunway Supply Chain Enterprises Sdn Bhd (“Sunway SCE”) for a consideration of RM167,589,760.00 (“Proposed Disposal”).

Premier Place and Sunway SCE will finalise and execute a Sale & Purchase Agreement (“SPA”) within 21 days from the date of the MoA. The SPA shall be conditional upon the approval of the shareholders of JRB for the Proposed Disposal.

Further details will be announced when the SPA is executed.

This announcement is dated 1 August 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 3-8-2017 05:29 AM

|

显示全部楼层

捷硕资源

售梳邦产业降债务

2017年8月3日

分析:大众投行研究

目标价:1.50令吉

最新进展

捷硕资源(JAKS,4723,主板建筑股)与双威(SUNWAY,5211,主板产业股)子公司双威供应链企业,签署协议备忘录,以1亿6758万9760令吉脱售位于雪兰莪梳邦的产业。

该产业占地约14.8英亩的工业地皮,目前为公司总部,在距离500米的范围,有大门广场、Summit USJ、Giant和Mydin霸级市场。

行家建议

每平方尺260令吉的脱售价,比我们预期的每平方尺300令吉,低13%,相信是因为目前的产业市场走软,以及改变发展计划。

假设公司只需支付产业盈利税和其他脱售成本,预计此次脱售,能带来1亿5500万令吉的现金。

脱售所得可用来改善资金流动,以及降低净债务。截至首季,净负债率达0.6倍。

捷硕资源原本计划在该地皮,发展捷硕大楼、3栋办公楼和6栋服务式公寓,预计发展总值为20亿令吉;但双威则计划,在该地皮发展总值14亿令吉的项目。

接下来,我们预计公司将会脱售Evolve Concept购物中心,不过目前该商场供过于求,相信短期不会脱售。

我们维持“中和”评级,目标价为1.50令吉。

【e南洋】 |

|

|

|

|

|

|

|

|

|

|

|

发表于 10-8-2017 04:42 AM

|

显示全部楼层

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

RELATED PARTY TRANSACTIONS | Description | Proposed Internal Reorganisation Involving Pacific Star Business Hub At Section 13, Petaling Jaya (Proposed Internal Reorganisation) | The Board of Directors of JAKS Resources Berhad (“JRB” or the “Company”) wishes to announce that the Company’s subsidiaries, JAKS Island Circle Sdn. Bhd. (“JIC”) and Fortress Pavilion Sdn. Bhd. (“FPSB”) have undertaken an internal reorganisation whereby, JIC had on 9 August 2017 entered into a Sale and Purchase Agreement (“SPA”) with FPSB for the sale of Pacific Star Business Hub (“the Property”) situated at Section 13, Petaling Jaya for a total consideration of RM240,000,000 (“the Purchase Price”).

For further details, Please refer to the attachment below.

This announcement is dated 9 August 2017. |

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5510857

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-8-2017 08:28 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3340

3340  62

62