|

|

发表于 26-10-2016 03:42 PM

|

显示全部楼层

发表于 26-10-2016 03:42 PM

|

显示全部楼层

本帖最后由 icy97 于 27-10-2016 12:07 AM 编辑

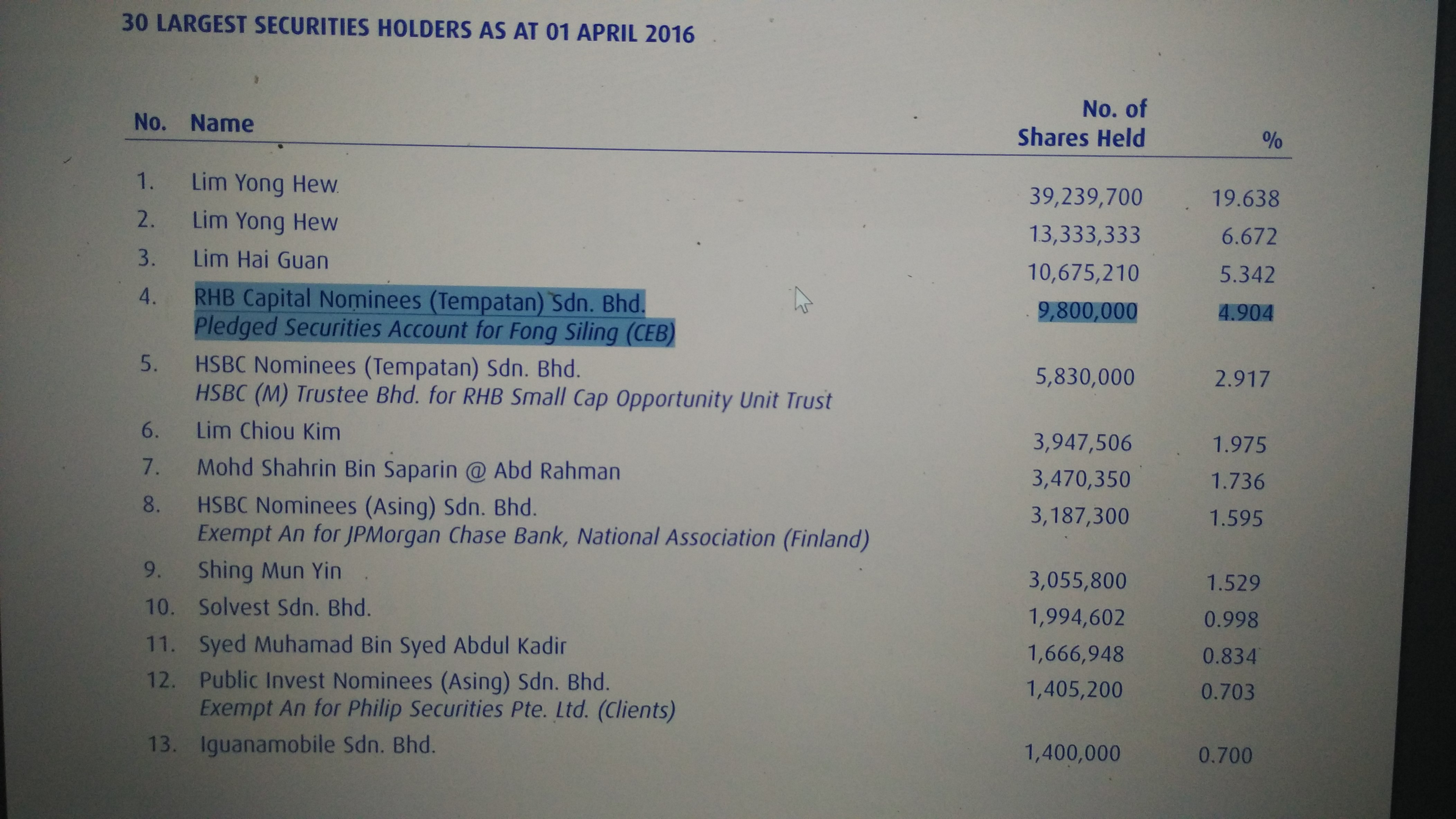

SOLUTN (0093) - Darling Of FongSiling (Cold Eye)

Author: wecan2088 | Publish date: Wed, 26 Oct 2016, 07:58 AM

http://klse.i3investor.com/blogs/solutnn/107217.jsp

SOLUTN is the darling stock of Fong Siling (Cold Eye). He bought the stock since year begining of year 2015. From the pic above, we know that Fong Siling hold substantial stakes 4.9% of SOLUTN. It is the biggest investment of Fong Siling. SOLUTN profit keep growing up every qtr. SOLUTN will announce its latest 3rd qtr results soon. It is likely a very good results.

SOLUTN yesterday up 1.5sen closed at 28sen.Technically it break 27.5sen strong resistance. It is likely will rise further and break new high due to 3rd qtr results will announce soon. Its 3rd qtr results will be very good one.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 26-10-2016 04:26 PM

|

显示全部楼层

哭哭鸟 发表于 26-10-2016 03:42 PM

SOLUTN (0093) - Darling Of FongSiling (Cold Eye)

SOLUTN is the darling stock of Fong Siling (Cold Eye). He bought the stock since year begining of year 2015. From the pic above, we know that Fo ...

原来冷眼也是top 5 shareholder

|

|

|

|

|

|

|

|

|

|

|

|

发表于 26-10-2016 04:29 PM

|

显示全部楼层

這已經是很久的事了..

|

|

|

|

|

|

|

|

|

|

|

|

发表于 27-10-2016 09:19 PM

|

显示全部楼层

Name

| Details of Changes | View

| Date

| Type

| No. of Shares

| Price

| LIM HAI GUAN | 20-Oct-2016 | Disposed | 50,000 | 0.000 | | LIM HAI GUAN | 20-Oct-2016 | Transferred | 2,500,000 | 0.000 | | LIM HAI GUAN | 18-Oct-2016 | Disposed | 1,500,000 | 0.000 | | LIM HAI GUAN | 17-Oct-2016 | Disposed | 500,000 | 0.000 | | LIM HAI GUAN | 13-Oct-2016 | Disposed | 500,000 | 0.000 | | LIM HAI GUAN | 13-Oct-2016 | Disposed | 500,000 | 0.000 | | LIM HAI GUAN | 12-Oct-2016 | Disposed | 2,000,000 | 0.000 | |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-11-2016 11:29 PM

|

显示全部楼层

本帖最后由 icy97 于 24-11-2016 12:19 AM 编辑

SUMMARY OF KEY FINANCIAL INFORMATION

30 Sep 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 30 Sep 2016 | 30 Sep 2015 | 30 Sep 2016 | 30 Sep 2015 | $$'000 | $$'000 | $$'000 | $$'000 |

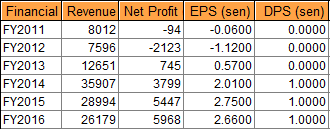

| 1 | Revenue | 10,162 | 5,962 | 26,179 | 20,765 | | 2 | Profit/(loss) before tax | 3,003 | 2,115 | 8,185 | 6,502 | | 3 | Profit/(loss) for the period | 2,263 | 1,546 | 6,263 | 4,518 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 2,083 | 1,473 | 5,966 | 4,246 | | 5 | Basic earnings/(loss) per share (Subunit) | 0.71 | 0.74 | 2.58 | 2.16 | | 6 | Proposed/Declared dividend per share (Subunit) | 1.00 | 0.00 | 1.00 | 1.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.1266 | 0.1583

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-11-2016 11:36 PM

|

显示全部楼层

本帖最后由 icy97 于 24-11-2016 12:21 AM 编辑

SOLUTN(0093)盈利再破新高,大方派息1仙!

Wednesday, November 23, 2016

http://harryteo.blogspot.my/2016/11/1380-solutn00931.html

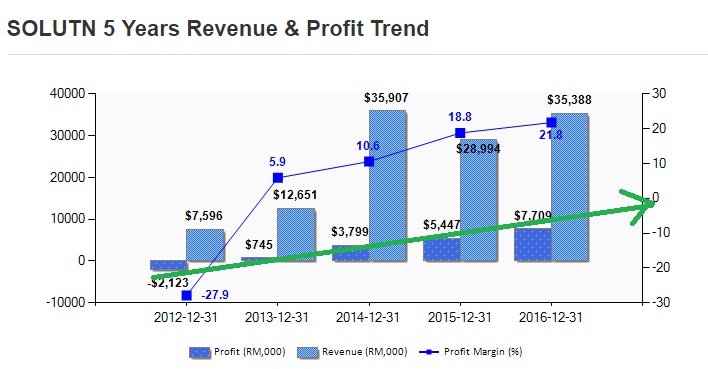

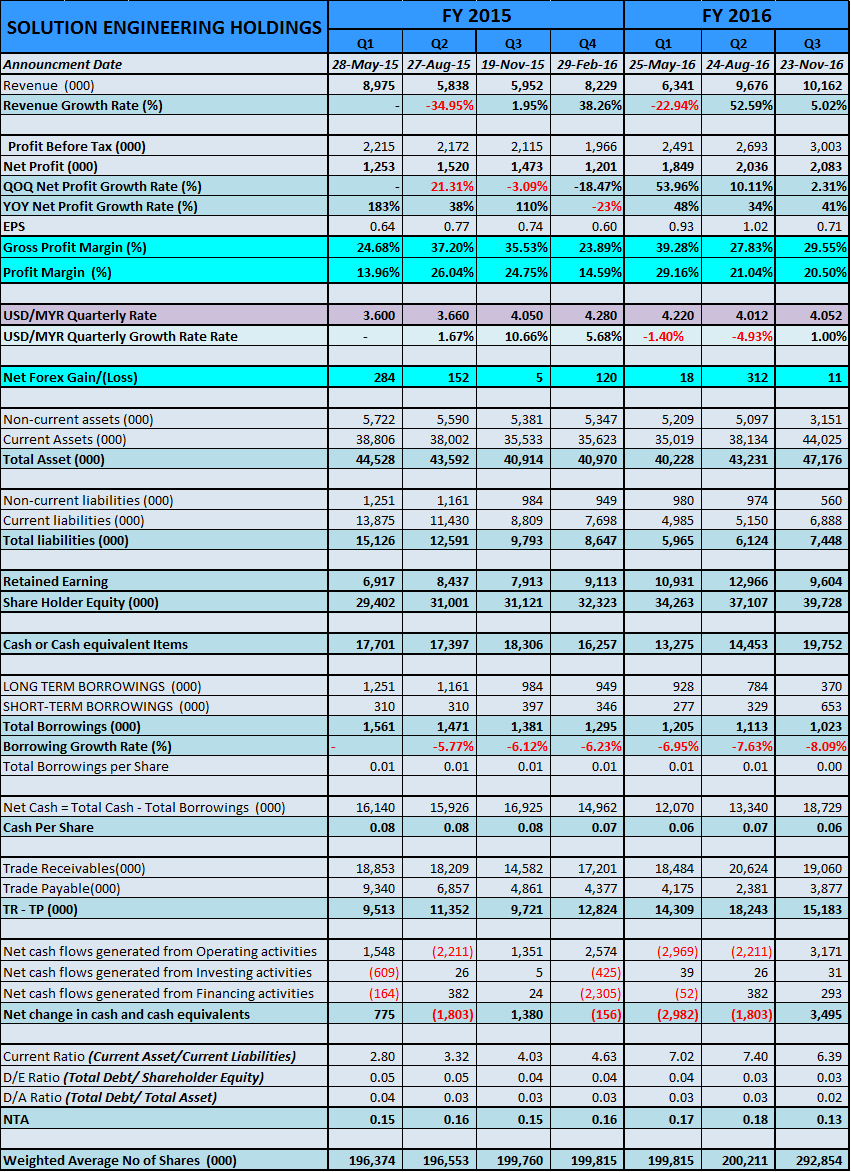

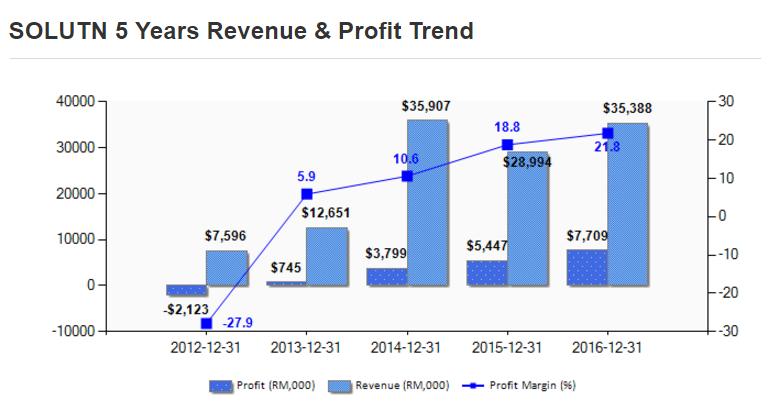

SOLUTN(0093)今天公布了非常出色的业绩,RM2.083 mil的Net Profit是历史新高。而且派发了1仙的股息,这相等于去年的1.5仙(今年2送1红股),所以股息按年增长了50%。此外,公司今年3个季度的Net Profit = 5.968 mil已经超过去年全年盈利的5.447 mil,今年的盈利按年应该有望成长40 - 50%。

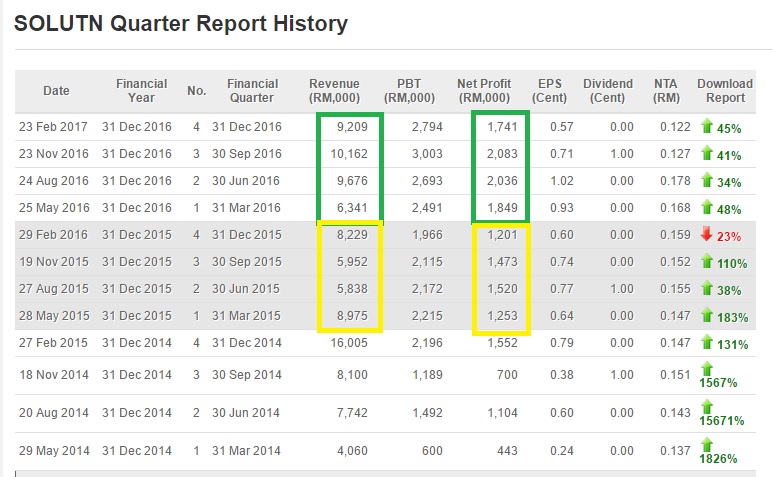

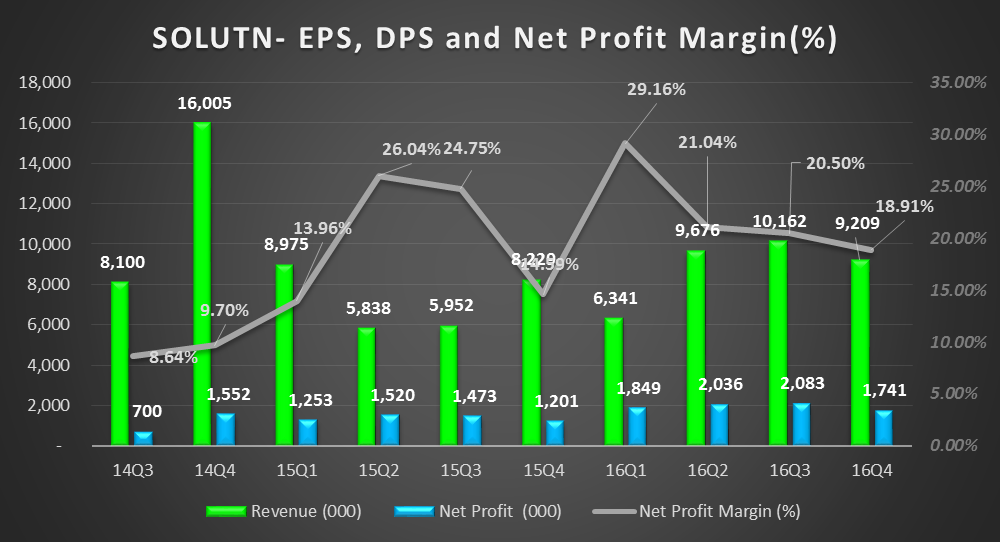

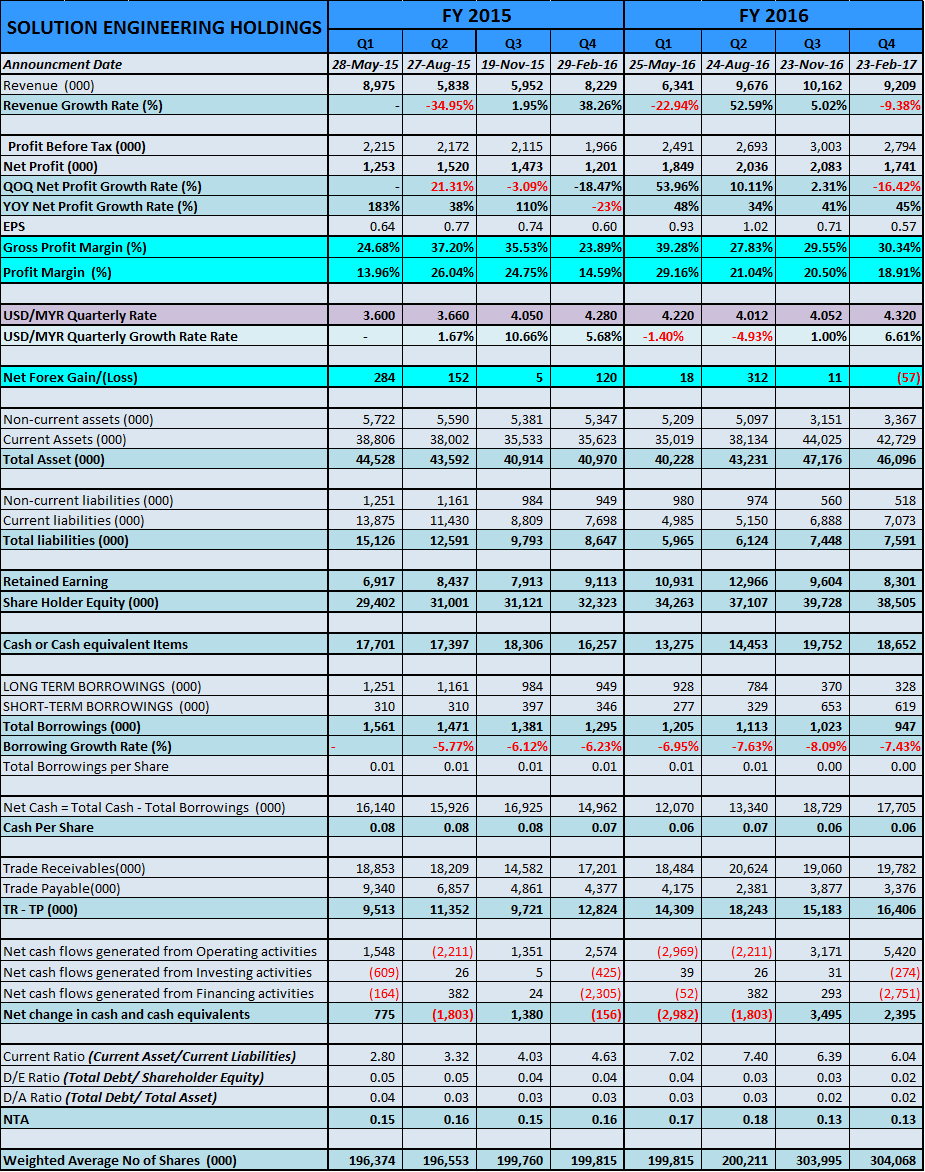

以下是SOLUTION过往7个季度的资产债务比表对比,希望对大家有帮助。

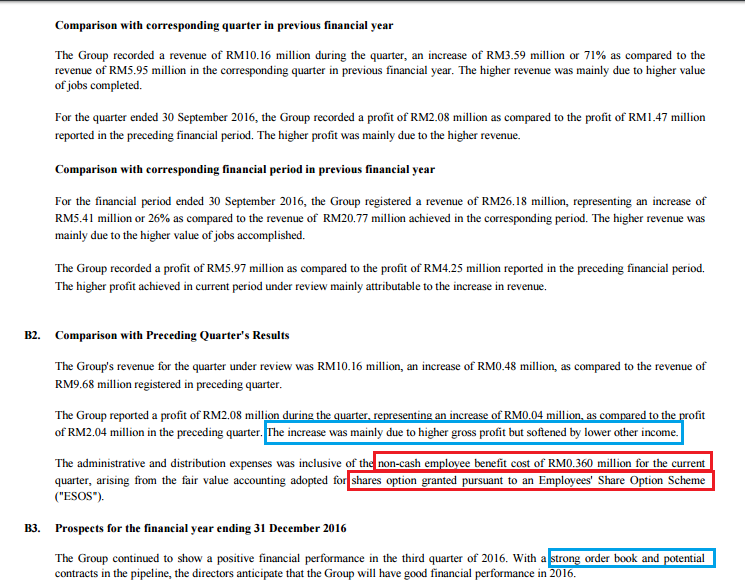

- SOLUTN的营业额比上个季度增长了5.02%,净利2.083 mil更是历史新高。

- 公司的Net Profit Margin已经连续3个季度保持在20%以上,最新季度的盈利下滑是因为0.36 mil的non -cash employee benefit cost,也就是所谓的ESOS。

- 假设撇除了ESOS, Net Profit至少会有2.2 mil以上,不过公司赚了钱,适度的奖励员工也是应该的。

- 公司的Cash in hand从14.453 mil进步到最新的19.752 mil,而Total Borrowing从1.113 mil减低到1.023 mil,债务降低了8.09%。净现金 = 18.729 mil,比上个季度的13.34 mil进步了足足5.4 mil。

- 以它手上的现金来看,SOLUTN明年的派息是有可能持续增加的。

- Gearing ratio保持在0.03超级低的水平,只要清还了所以债务,SOLUTN就可以变成【0债务】公司。

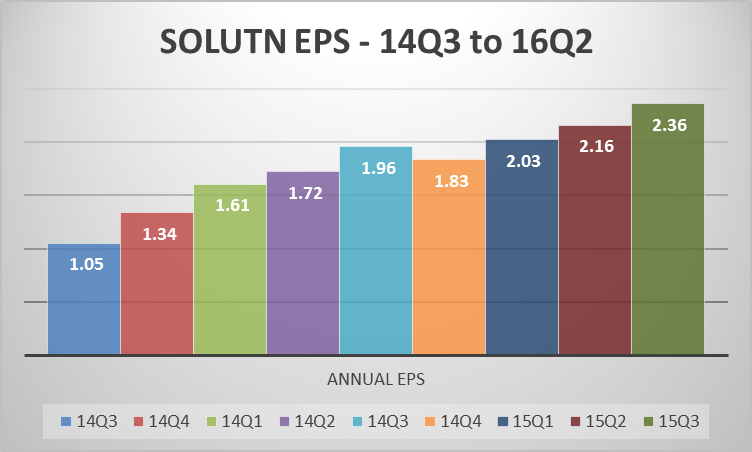

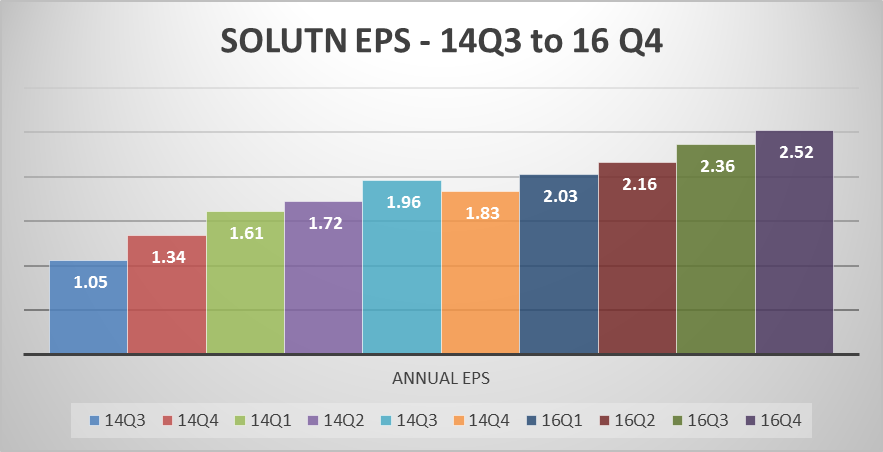

上图是SOLUTN最近9个季度的全年盈利,SOLUTN在公布了业绩之后,EPS从上个季度的2.16成长到2.36仙,成长了9.26%.

公司今年3个季度的盈利都保持成长,去年Q4的盈利只有1.201 mil,2016Q4要保持YOY盈利成长40%应该不是难事。

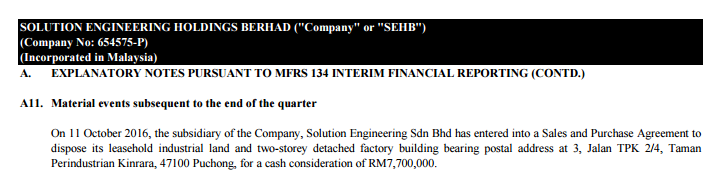

公司之前公布卖出建筑物在明年将会获得7.7 mil的现金,因此SOLUTN的现金流在明年会变得更加宽松,很有可能会派发更高的股息来回馈股东们。

从上图的报告解说,公司的因为营业额增长而促进的盈利上涨。不过0.36 mil的ESOS expenses却拉低了盈利,不然net profit可以再进步10%左右。

公司手握不菲的合约,它们也在竞标着新的工程,因此公司对今年Q4的盈利保持乐观。以现在31仙的股价计算,1仙的股息相等于3.22%的周息率。假设是在10月头以25仙买进,周息率高达4%。

不过股价在短短的一个月内上涨了接近30%,所以股价有可能会在业绩的利好因素出炉后而被散户套利。以价值基本面的角度分析,SOLUTN是一家长期盈利成长的公司,明年还有5.4 mil的卖地盈利进账。所以可以肯定的是,今年的盈利已经优秀过去年,明年的盈利也将会高过今年,这种公司在马股应该很难找了。

以上纯属分享,买卖请自负。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 28-11-2016 12:26 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 2-12-2016 04:50 AM

|

显示全部楼层

EX-date | 08 Dec 2016 | Entitlement date | 13 Dec 2016 | Entitlement time | 05:00 PM | Entitlement subject | Interim Dividend | Entitlement description | An Interim Single-tier Tax-exempt Dividend of 1.0 sen per ordinary share for the financial year ending 31 December 2016 | Period of interest payment | to | Financial Year End | 31 Dec 2016 | Share transfer book & register of members will be | 13 Dec 2016 to 13 Dec 2016 closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | Tricor Investor & Issuing House Services Sdn BhdUnit 32-01, Level 32, Tower AVertical Business Suite, Avenue 3Bangsar South, No.8 Jalan Kerinchi59200 Kuala Lumpur, Malaysia.Tel: +6(03) 2783 9299 Fax: +6(03) 2783 9222 | Payment date | 23 Dec 2016 | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 13 Dec 2016 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) |

| | Entitlement indicator | Currency | Currency | Malaysian Ringgit (MYR) | Entitlement in Currency | 0.01 | Par Value | Malaysian Ringgit (MYR) 0.100 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-12-2016 11:42 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 15-12-2016 07:15 PM

|

显示全部楼层

本帖最后由 icy97 于 16-12-2016 01:09 AM 编辑

冷眼推荐股(二十三):SOLUTN

Thursday, December 15, 2016

http://bblifediary.blogspot.my/2016/12/solutn.html

业务

- 设计、制造与提供教学与研究器材

- 矽硼玻璃实验装置和零件销售

- 汽车润滑剂销售

SOLUTION(方案工程控股,0093,创业版科技股),成立于1988年,并于2005年上市大马交易所创业板。

SOLUTN是一家投资控股公司,涉足专业教育领域的科技公司,该公司有一个非常特别的核心业务,那就是为教育机构(如私人或政府大学、学院、技术培训中心等)设计、订制和开发各种各样的教学与研究设备和器材。

自从该公司上市之后,凭借着上市地位的优势,如今已经发展成为国内和本区域具有领导地位的教学与研究器材生产和销售公司。

SOLUTN是以SOLTEQ、SOLDAS及SOLCAL品牌在国内及海外教学与研究器材市场建立起良好的信誉。

目前除了国内大部份的政府和私立教育机构向公司订购教学与研究器材之外,海外订单也有不断增加的趋势,这些订单包括来自非洲、中东、东南亚等地。目前,该公司也在超过30个国家拥有分销商。

SOLUTN也是德国矽硼玻璃试验装置和零件制造商QVF的独家分销商,矽硼玻璃试验装置主要应用在实验室、研发和工业生产层面。

除了生产和销售教学与研究器材的核心业务,方案工程也通过子公司从事生产及销售工业及汽车润滑油添加剂、生物反应器及生物加工仪器以及工业自动化设备的业务。

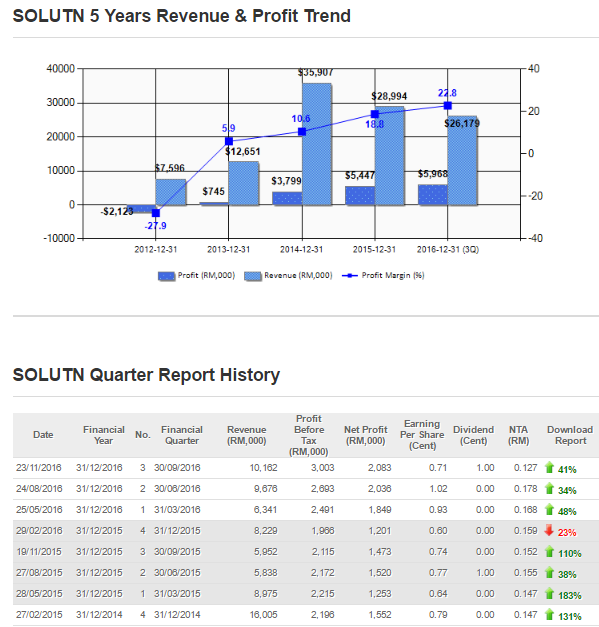

SOLUTN这几年的业绩表现算是不错的,自2013年转亏为盈后,净利就每年增加。且公司在迈入2016年后,业绩出现大跃进。

在截至2016年9月30日为止,SOLUTN的净利达到597万令吉,已经超越去年的545万令吉。预料第四季的净利可以达到200万令吉以上,那么2016年全年净利将有望达到历史新高的800万令吉。(注:该公司6月刚完成2送1红股,每股净利将冲淡至1.68仙左右)

SOLUTN有计划在未来转至主板挂牌,要达到这个目标公司就必须继续把营业额和净利推高,这样才能够符合转板条件,因此确实让人期待。

免责声明:

以上投资分析,纯属本人个人意见和观点。

文章所提做出的数据与价格仅供参考,建议大家在买进一家公司的股份前,请先做功课并了解该公司,并衡量应何时进场和离场,任何人因看此文章而造成任何投资损失,本人恕不负责。切记,买卖自负!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 24-1-2017 11:38 AM

|

显示全部楼层

本帖最后由 icy97 于 25-1-2017 12:46 AM 编辑

SOLUTN - Solution for Education (B)

Author: Stockify | Publish date: Mon, 23 Jan 2017, 07:14 PM

http://klse.i3investor.com/blogs/stockify/114508.jsp

Introduction

Solution Engineering Holdings Bhd (SEHB) is one of the top 30 stockpick by the Malaysia infamous investor, Mr. Fong Siling AKA Coldeye. This has drawn our attention to find out more about the company. While searching online about the company, we noticed that most of the write-ups about SEHB did not explain much about the business. Today, we will cover as much as we can on the group’s main business, and its services/products.

Let us start with some brief introduction. The SEHB was incorporated in 2004 and was public listed in Bursa Ace Market (formerly known as MESDAQ market) on the same year. Initially, SEHB was mainly designing and developing hardware and software for engineering education and research for high education institutions. Over the years, they have been focusing on the R&D, which eventually results with wide range of products and simulation modules. They have also expanded their education and research products into biotechnology and pharmaceutical field. Today, the group is involved in several business areas:

1) Educational engineering equipment 2) Production and distribution of lubricants 3) Provision of industrial biotechnology 4) Automation solution provider.

Business

Education Equipment The educational engineering equipment business has been the group’s core business. The engineering equipment division has contributed 80% of the overall revenue in 2014. The operations of Solution Engineering Sdn Bhd involved design and develop equipment for engineering education and research as well Technical Vocational Education and Training (TVET). Currently, the company has 3 major products: SOLTEQ, SOLDAS and SOLCAL.

SOLTEQ involves wide range of engineering education equipment, which can be categorised into: - Process Control - Heat Transfer & Thermodynamics - Fluid Mechanics - Environmental Engineering - Chemical & Bioprocess Engineering Pilot Plants - Basic Process & Reaction Engineering

Air Conditioning Laboratory Unit (Model AC 01)

Boiler Heating Batching Control Trainer (Model SE 107)

Each education equipment is specifically designed to represent real life engineering system in lab scale, which allows engineering students or researchers to experiment through simulations. Education equipment are supplied along with process control instruments such as switches, gauges, transmitters, control valves, process controllers, and alarms. The client is given an option to include data acquisition system (SOLDAS) and computer aided learning software (SOLCAL) in their purchase.

GUI of SOLDAS Data Acquisition System

SOLDAS data acquisition system includes the following in its package:

- A PC with latest Pentium Processor

- An electronic signal conditioning system

- Standalone data acquisition modules

- Window based data acquisition software for data logging, signal analysis, process control, real-time display, tabulated results, plotting graphs.

SOLCAL Computer Aided Learning Software

On the other hand, SOLCAL Computer Aided Learning Software comes with the following items: - Interactive multimedia features - Graphical simulation - Experimental results samples - Full experimental manuals

Judging from the functions of the two optional products, it is logic to think that the two “optional" products are somewhat necessary and very likely to be purchased with the experimental-based-equipment, which is good sales strategy. As we can see from its product catalogue, wide range of engineering education equipment are mostly supplied as a complete engineering system, we opine that the equipment components, SOLDAS and SOLCAL are the main inventories, while the SOLEQ equipment are likely to be manufactured/assembled upon purchase order/contract and also the major sales contributor. Hence, we assume the education equipment sales are mostly on contract basis.

Biotechnology The main products of SBSB are bioreactor and fermentor for modelling various microbial (bacteria, yeast, fungi) culture processes.

The Group’s biotechnology segment is operated under its subsidiary, Solution Bioforce Sdn Bhd (SBSB), which specialises in Biotechnology and Pharmaceutical, provides engineering solutions, design / development of biopharma equipment. Incorporated in 2011.

The available product series are: - BLF series: Basic series for small scale production, education and research, available in 1 - 10 L capacity. - CLF series: Compact series for small scale production, education and research, available in 1 - 14 L capacity. - PLF series: Modular, predesign and configured turnkey system for research to small scale production, available in 10 - 5,000L capacity. - BTU series: Teaching unit series for education.

Bioreactor series

All bioreactor series, except for BTU series are supplied as a package inclusive of other components such as bioreactor system, heating system, process vessels, software, measurements and control system. Pumps, SIP (sterilised) and CIP (cleaning) systems are only included in the PLF supply package for its pilot plant scale.

Lubricant The lubricant business operates under Solution Biogen Sdn Bhd contributes 5% of the group’s revenue in FY14. This subsidiary is acquired by Solution Engineering Holdings Sdn Bhd in 2013. The company mainly produces local Malaysia brand lubricants, which are biodegradable and made of esters and other palm oil products. Their lubricant products are categorised into 4 major types: automotive engine oils, heavy duty diesel engine oils, marine oils, and motorcycle engine oils. In 2012, the company is also started to supply Viscosity Index Improvers (VII), which commonly used in multigrade engine oils, gear oils, automatic transmission fluids, power steering fluids, greases and hydraulic fluids.

SOLMAX Lubricants

SCADA & Automation SystemThis business area is operated under Solution A&C Technology Sdn Bhd in which the Group owned 70% of shareholding. This subsidiary specialised in SCADA (Supervisory Control and Data Acquisition) & Automation system. The company has participated in River of Life (RoL) project as automation system provider. The project aims to transform the polluted Klang River to high economic value environment by river cleaning and beautification.

Business Analysis

One of the reasons that it caught our attention to study further is its high gross profit margin of ~50% and net profit margin of ~20%. Considering the core business, Educational equipment division, it is hard to imagine supplying engineering equipment to education institution could yield such impressive margin. From the previous explanation of the group’s equipment business, we noticed that using “equipment” to describe the products could be misleading, we would prefer to describe the products as “system”. Here is the reason, many would think that the educational equipment is sold as a single item in which common equipment business does. In the case of SEHB, their product is the assembly of many components such as vessels, control instruments, switches, gauges, transmitters, control valves, PID controllers, alarms, SOLDAS, and SOLCAL based on their process design blueprint. The process design blueprints are the results of the invested R&D, which brings values to its equipment. Hence, this explains why the educational equipment business yields high profit margin.

Apart from that, automation solution provider is a service business, which requires certain human expertise to “assemble” various automation instruments to create values to the customers. Hence, it could be one of the contributors to the high profit margin of the group.

However, looking at the revenue segment of the Group, 99% of the revenue in 2015 is contributed by contracts and the remaining is from sales of goods, this could mean most of the group’s income is non-recurring. For instance, it is not likely for the education institution to purchase the similar education equipment every year, unless for uncommon reasons such as expansion, but it is likely that certain components of the equipment will be purchased for maintenance purpose. Hence, this explains why sales of goods has little contribution to the revenue, compare to the contract sales.

Growth driver As mentioned previously, the core business of the group comes from engineering educational equipment business. In 2016Q3 (TTM), we estimated that the top line contribution from overseas has declined from RM 5.2 mil in 2014 to the latest RM 2.4 mil, which is 7% of the overall revenue. Hence, the group’s revenue is mainly on domestic education market. In 2015, Malaysia has 410 private higher education institutions nationwide. The government is aiming to create 1.5 mil jobs in the year 2020 under 11th Malaysia Plan (RMK11), where 60% of the jobs will require Technical Vocational Education and Training (TVET) skills. The initiative is of good purpose to shift working society from labour intensive to knowledge and innovative based jobs. To make this happens, the TVET sector has to increase its annual intake from 164,000 in 2013 to 225,000 in 2020. As mentioned by the management, their educational equipment business will be one of the beneficiaries of this government initiative. Apart from that, the management has the intention to invest in R&D to improve their products to adopt the green and renewable technologies.

Conclusion

To conclude this, readers from non-engineering background might find it difficult to understand the products and services of Solution Engineering Holdings. We would like to say it is absolutely normal, as the business model is based on engineering knowledge. Hence, investors are expected to require some engineering and technical experience to understand the business. We always believed that investing in business within the Cycle of Competence is important in investing. We believe that margin of safety does not merely come from valuation alone, it also comes from the qualitative aspect of a business.

References:

|

|

|

|

|

|

|

|

|

|

|

|

发表于 6-2-2017 11:32 PM

|

显示全部楼层

[SOLUTION Group] - Groundbreaking Ceremony

A 3 storey production facilities and office building at Technology Park Malaysia.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-2-2017 12:27 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 13-2-2017 01:17 AM

|

显示全部楼层

本帖最后由 icy97 于 13-2-2017 02:03 AM 编辑

SOLUTN - Solution for Education (F)

Author: Stockify | Publish date: Sun, 12 Feb 2017, 08:42 PM

http://klse.i3investor.com/blogs/stockify/115652.jsp

In previous post, we explored the business model of SOLUTN. In this post, we will look at SOLUTN (0093) financial numbers to understand more about its company financial and its business performance from income statement, balance sheet, and cash flow statement. Finally, we will do a valuation to determine if the current price is a good bargain. To begin, we always believe that

“In the business world, the rear-view mirror is always clearer than the windshield. - Warren Buffett”, so while doing our research, we prefer to start by looking at the past performance of the company over the years.

Income Statement The basic requirement of a good business is to make money. So how did Solutn perform for the past 5 years? From the past record, the business performance of the company was not impressive before FY13. Anyone who invested in the company before FY13, must have strong faith in the management. So what has happened to the company in FY11-FY12?

In FY11, the company has posted 11.3 mil Revenue (-38% YoY) and 0.4 mil net profit (-81% YoY) due to "lower sales of SOLEQ equipment projects recognised and also lower profit margin in certain R&D projects - Annual Report 2011”. Apart from that, in the FY11 Q4 quarterly report, it was clearly stated that the company has unusual high Administration and Distribution cost, because of provision of RM 300,000 for fire damage, which was an one-off loss.

Taken from Solution FY11 Q4 financial report

In FY12, the company’s financial performance continued to drop by posting a revenue of 7.9 mil (-31% YoY) and making a net loss of -2.1mil. The management put their blame of the disappointing performance on competitive business environment and reduced government budget. Another reason was due to the write off of subsidiary development expenditure that was about 2 mil.

Taken from FY12 Q4 financial report

Taken from FY12 Annual Report

Though there were some one-off items during this difficult period, we do think that these are acceptable, while 300k fire damage provision was insignificant too. High percentage of Administration and Distribution costs during low revenue period are the real culprits that caused loss to the company. In FY11, the admin and distribution costs was about 28% of the revenue, while in FY12, it surged up to 52% after excluding the 2 mil write off expenses, mainly due to the lower revenue in the year, which led to EBIT (Earning Before Interest and Tax) of -2.1 mil. We believed the management was aware of this during that time, and has been working hard to be more cost-effective and productive in operating their business. The company has started to turnaround its business in FY13, where its EBIT has seen to improve slightly to 0.74 mil net profit. This was mainly due to effective cost control in project contracts by the management and also sales of a new product development.

As a result of the management’s effort in improving sales of their equipment segment and venture into various businesses (biotech, automation), the company has now recorded 34.5 mil sales, resulting with 7.1 mil net profit and achieving impressive net profit margin of 20.7% in FY16 Q3 (TTM). In overall, the company has given impressive growth of 25% CAGR on its revenue and 78.5% CAGR on its net profit over the past 5 years.

Illustration 1 - Profitability data from FY11 - FY16 Q3 (TTM)

Illustration 2 - Profitability from FY11 - FY16 Q3 (TTM)

Illustration 3 - Profit Margin from FY11 to FY16 Q3 (TTM)

Considering volatility of MYR in recent years, one would like to know if the company’s main revenue is from domestic or foreign market. Illustration 3 shows that the main revenue contribution is predominantly from domestic market (93%) and 7% from overseas in the latest FY16 Q3 (TTM). The company has shown significant sales growth in domestic market, while overseas market remains flat.

Illustration 4 - Segmental revenue from FY11 - FY16 Q3 (TTM)

Illustration 5 - Geographical distribution of Revenue in FY16 Q3 (TTM)

As mentioned previously, majority of the sales is from contract based works and projects, which are non-recurring. In FY15, the contract based revenue has contributed 99% of the total revenue, worth 28.7mil, while only 1% came from the sales of goods. Illustration 6 shows that the contract revenue has grown significantly over the years. However, the management only mentioned that they are backed with strong order book without providing actual figure for it. Due to its business nature, we think it is important for the company to reveal their current order book to the public, to figure out the sustainability of their business. Despite of the lack of information, the financial number tells us that the current performance company is impressive.

Illustration 6 - Sources of Revenue from FY11 - FY15

Balance Sheet Now, let us dive into the balance sheet to see how’s the financial health of the company. As an investor, the last thing we would like to do is investing in company that is facing financial difficulty and near to bankruptcy any soon, as this will expose ourselves to high risk. We prefer company with no/low debt, net cash, good liquidity ratios (current ratio, quick ratio, cash ratio).

Illustration 7 - Liquidity ratios

Illustration 8 - Key data extracted from Balance Sheet

From the figures, we find how amazing that SOLUTN is able to keep their healthy balance sheet over the years despite of those tough sales years. From Illustration 8, we can see that the management has been keeping their debts low to avoid the double edge effect of the leverage in their business. One notable highlight is their cash & securities have been growing from 8.4 mil (FY11) to 19.8 mil (FY16 Q3), which represents a CAGR of 20% over 5 years period. This indicates that real cash AKA Free Cash Flow (FCF) is generating from their operation. Having relatively huge pile of cash in hand, the company is currently a net cash company. All liquidity ratios such as current ratio, quick ratio, and cash ratio, have been at healthy level, which tell us that the company will not face any financial issue with this strong balance sheet. One might ask, why is the cash per share has dropped to 6 cents per share in FY16 Q3, this is due to dilution from 1:2 bonus issue last year. In overall, we are happy with the balance sheet of the company as it lowers the investment risks.

Cash Flow Statement Cash flow is like the blood circulation system of a company. A healthy business should be able to generate cash from its operation after spending on necessary CAPEX. We prefer company that has shown consistent CFFO (Cash Flow From Operation) with low CAPEX (Capital Expenditures), which leads to positive FCF (Free Cash Flow). Regardless of the profitability, the objective is to generate real cash from the business operation alone, which shows how important it is to look at the CFFO. Low CAPEX may indicate that the business is not capital intensive and its easier to manage with low capital requirement. Company that has positive FCF will show increasing cash in hand, which can be used for dividend payout to reward its shareholders or spend on acquisition new PPE or businesses. In the case of SOLUTN, we see inconsistent CFFO over the past 5 years. However, one thing that we can observe from the past is that the business is not capital intensive as shown by the consistently low CAPEX in the past. We hope to see more consistent cash flow from the company in the future.

Illustration 9 - CFFO, CAPEX and FCF

Illustration 10 - Cash Flow Checklists

Based on our own cash flow checklists, we rate the cash flow condition of SOLUTN as AVERAGE.

Management It is undeniable that good management is a plus to both the company and investors. However, evaluation of the management is mostly requires qualitative and subjective. Nevertheless, there are few quantitative metrics that can provide some information about the efficiency of the management. We will be looking at the ROE (Return on Equity), ROIC (Return on Invested Capital), CROIC (Cash Return on Invested Capital) and ROA (Return on Assets).

Illustration 11 - Efficiency ratios from FY11 to FY16 Q3

From Illustration 9, 3 of the efficiency ratios, ROE, ROIC, and ROA have been increasing consistently annually after the terrible FY12. This is a good sign that showing that the company is being well managed, especially in latest FY16 Q3, the company has recorded 18% ROE, 41% ROIC and 15% ROA. High ROIC as such tells us that the company might have certain level of competitive advantage in the industry.

ROE can tell us how efficient is the management in generating profit for the shareholders, but it can be easily distorted by financial leverage. Hence, we would like to breakdown ROE into 3 components: Financial Leverage, Asset Turnover, and Net profit margin. We can see from Illustration 10 that the improving ROE is mainly attribute to higher asset turnover and improvement in net profit margin, which is desirable.

Illustration 12 - DuPont Analysis

ROA tells us how much profit the company has made for every dollar of its assets. The past ROA tells us that the company has been consistently improving its utilization of assets over the years, which is a good sign. Finally, it comes to the CROIC of the company. Its CROIC is inconsistent and fluctuated over the past years, this is due to inconsistent CFFO (Cash Flow From Operation) especially in FY15. This was caused by huge reduction in trade payables. We hope to see more stable and consistent CROIC from the company. After all, we would like to remind our readers that these metrics would be more useful to compare against peers, which we couldn’t identify any at the moment.

Valuation Till the end of the day, a good investment is pretty much depending on the price versus value of the company. We prefer to invest with sufficient Margin of Safety to lower the downside of an investment. There are various valuation tools that can be used to value the company. First of all, we used some of the common relative valuation metrics to have a quick check on the current valuation based on the latest closing price at 0.340 on 10/02/2017.

Illustration 13 - Common Relative Valuation metrics

From Illustration 13, the relative valuation metrics show that the current price does not seem to be attractive. Please note that the metrics are compared against general benchmark as a reference. We think the company is currently at fast growth stage, hence, we may attempt a valuation based on PEG ratio, that is popularized by the legendary fund manager, Peter Lynch.

Illustration 14 - PEG valuation

In Peter Lynch’s book "One Up On Wall Street”, he mentioned that a PE ratio that is half of the growth rate is a bargain, PE that is equal to the growth rate is fairly priced, while PE that is double of growth rate is overly priced. In this case, we will try to check on the PEG based on different growth assumptions. We found that based on the 5-year CAGR at 78.5%, the PEG is only 0.18, which is undervalued. However, based on lack of information revealed by the management about the future growth, we think it is over-optimistic to think that the company is able to sustain their growth at 78.5% without the support of strong evidence or details, thus, this is known as the BEST case. In BASEcase scenario, we applied a reverse engineering from 0.5 PEG, we found that the current price is undervalued if the company is able to keep its earning growth at 29%. In WORST case, if the company’s earning growth is at 15%, the current price is fairly valued by the market.

Conclusion To conclude this financial post, we find SOLUTN to be a company with good fundamental, which has low likelihood of facing any financial issue in near term, which further backed by its net cash position. In term of profitability, the company has shown remarkable net profit growth at 78.5% CAGR, which mainly contributed from domestic market. However, the cash flow of the company has not been consistent over the past 5 years. Apart from that, various efficiency ratios have also shown that the capability of the management in improving its operation efficiency and productivity. Finally, based on the PEG valuation approach, the company appears to be undervalued, but given the lack of information disclosed by the management, we do not like to be overly optimistic in their future growth, we would like to have clearer evidence to conclude the current valuation of the company. |

|

|

|

|

|

|

|

|

|

|

|

发表于 23-2-2017 07:32 PM

|

显示全部楼层

本帖最后由 icy97 于 24-2-2017 12:57 AM 编辑

SUMMARY OF KEY FINANCIAL INFORMATION

31 Dec 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 31 Dec 2016 | 31 Dec 2015 | 31 Dec 2016 | 31 Dec 2015 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 9,209 | 8,229 | 35,388 | 29,073 | | 2 | Profit/(loss) before tax | 2,794 | 1,996 | 10,979 | 8,450 | | 3 | Profit/(loss) for the period | 1,746 | 1,225 | 8,009 | 5,730 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 1,741 | 1,201 | 7,707 | 5,415 | | 5 | Basic earnings/(loss) per share (Subunit) | 0.57 | 0.74 | 3.09 | 2.74 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 1.00 | 1.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.1224 | 0.1583

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 24-2-2017 01:00 AM

|

显示全部楼层

本帖最后由 icy97 于 24-2-2017 02:18 AM 编辑

【价值仙股】- SOLUTN(0093)盈利YOY进步45%,FY17稳定成长!

Thursday, February 23, 2017

http://harryteo.blogspot.my/2017/02/1390-solutn0093yoy45fy17.html

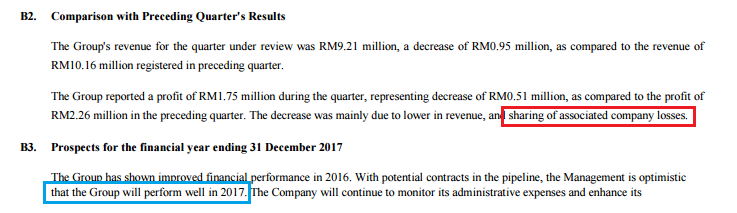

SOLUTN(0093)最新季度的营业额以及盈利YOY分别进步了12%以及45%。整体来说业绩是【中规中矩】,因为这个季度的盈利是4个季度里最差的。这跟去年的情况很相似,Q4连续两年成为最差的季度。不过全年来比较的话,盈利全年进步了42%,这样的成长是值得嘉许的。

SOLUTN的盈利已经连续4年保持成长,管理层可说是交出了非常出色的答案卷。而最新季度的Net Profit Margin更是进步到21.8%,是近年的新高。

虽然这个季度的盈利放缓,但是以全年EPS来看,公司这个季度从16Q3的2.34仙进步到最新的2.52仙,现在还是处于历史新高的盈利。

- SOLUTN的资产债务表其实非常简单,Cash Position = RM18.652 mil,借贷减低到RM947K, 净现金 = RM17.705 mil。

- 现金减少是因为FY16派发了1仙的股息,相等于RM3.04 mil。

- 而Trade Payable从上个季度的RM3.877 mil下滑到RM3.376 mil,可以见到管理层非常努力在减少公司的Liabilities。

- 卖掉旧厂的一次性收入预计会在下半年进账,现金流在未来会变得更加强劲。

总结:

这次盈利减少主要是因为营业额减少以及Sharing of associated company losses = RM89,000。不过管理层在展望里写到,公司会perform 【WELL】 in 2017,因此笔者预计FY17还是可以保持稳定的成长。

公司的股价从年头的0.305上涨到今天的34仙,涨幅是11.48%,之前一度突破历史新高35分。假设以9月30日低谷的股价24仙为准,SOLUTN股价在5个月内上涨超过40%,这还不包括1仙的股息。股价最近有点过热的迹象,因此短期出现套利回调的显现也不足以为奇。

假设公司可以保持20%的盈利成长+ 额外的1.78 EPS,SOLUTN未来的表现还是值得期待的。不过这家公司未来需要一点耐心,需要长期持有才能看到成绩。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 17-3-2017 07:44 PM

|

显示全部楼层

本帖最后由 icy97 于 18-3-2017 12:02 AM 编辑

Solutn - Three reasons make stock price heading north

Author: BursaButterfly | Publish date: Fri, 17 Mar 2017, 12:12 AM

https://klse.i3investor.com/blogs/bbcstock/118490.jsp

Solution Engineering Holdings Berhad (SEHB) is a Malaysia-based company engaged in investment holding and provision of management services. The Company, through its subsidiaries, is engaged in designing and development of equipment for bio-lubricant project and for engineering education and research and provision of training and curriculum content development. SEHB products are utilized in public and private universities, university colleges, polytechnics, skilled training centers, advanced technical institutions and colleges. Its subsidiaries are Solution Engineering Sdn. Bhd., Solution Biogen Sdn. Bhd., and Solution E & E Technology Sdn. Bhd.

There are three reasons that will make the stock price heading north:

- Strong fundamental

-Cold eye is major shareholder

-Diposal High EPS coming in FY17

FUNDAMENTAL

The growth in net profit for the past 5 years showing that the company is puttig hardwork to improve its profit margin, controlling the administration&distibution expenses. Comparing FY16, the company revenue so recovering back from GST impact last year, where the profit margin has record high in he history. The profit margin has achieve as high as 21.8%, purely from operating business, without any other income which is rarely found in ACE listed company

Solution quarter results in terms of revenue and net profit, showing great improvement over quarters, this figures have confirmed that Solution Engineering Bhd is a growth company, based on the growth rate, we are expecting revenue of RM40millions in FY17. In addition, solutn is very generous to give out dividend each year to attract investor attentions.

"From the figures, we find how amazing that SOLUTN is able to keep their healthy balance sheet over the years despite of those tough sales years. From Illustration 8, we can see that the management has been keeping their debts low to avoid the double edge effect of the leverage in their business. One notable highlight is their cash & securities have been growing from 8.4 mil (FY11) to 19.8 mil (FY16 Q3), which represents a CAGR of 20% over 5 years period. This indicates that real cash AKA Free Cash Flow (FCF) is generating from their operation. Having relatively huge pile of cash in hand, the company is currently a net cash company. All liquidity ratios such as current ratio, quick ratio, and cash ratio, have been at healthy level, which tell us that the company will not face any financial issue with this strong balance sheet. One might ask, why is the cash per share has dropped to 6 cents per share in FY16 Q3, this is due to dilution from 1:2 bonus issue last year. In overall, we are happy with the balance sheet of the company as it lowers the investment risks." From Author: Stockify http://klse.i3investor.com/blogs/stockify/115652.jsp

Major Shareholder

Solution also is one of the stockpick by Malaysia most famous fundamental investor, Mr. Fong siling AKA Coldeye. He has 9.8million shares or 4.9%, third largest major shareholder in the company, right after both company Director, Mr. Lim Yong Yew and Mr. Lim Hai Guan.

Mr. Fong siling AKA Coldeye, The largest pure investor in solutn

Coldeye will only sell out this shares when the stock is overpricing or fundamental turns bad. From the current stock prices, PE ratio, company growth rate and balance sheet, we believe that Coldeye is still holding high stake of solutn share.

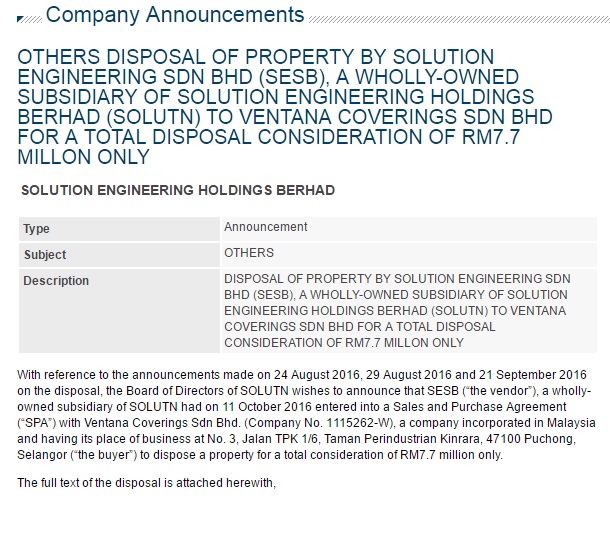

Disposal of property

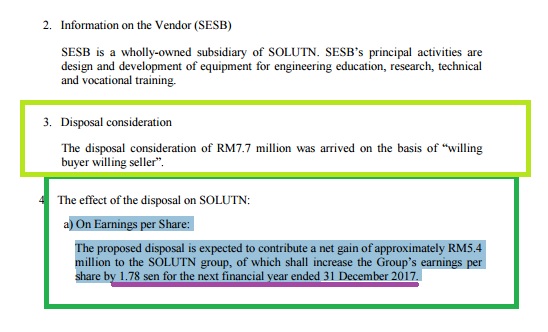

In 2016 Oct, the company entered into SPA with Ventana Covering Sdn Bhd. , agreed to dispose a property for RM7.7 million, this figure will be reflecting in FY17

Solutn has approximately RM5.4 million or EPS 1.78 eps coming soon in FY17. So, if we considering the company operating latest EPS is 2.52 sens, if the results in FY17 could maintain at this figure, this means 2.52+1.78 = 4.3sens, which means in FY17 solutn earning per share will achieve 70% higher compared to FY16

From the chart above, the stock prices had been staying horizontal after bonus issue in 2016, then huge trading volume occurs in Oct 16 which trigger the stock price to move north, begins its first uptrend after bonus issue.

Its expecting this uptrend and current market sentiment, which is very bullist now, will continue to move up to above RM0.45, the price before bonus issue.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-3-2017 02:44 PM

|

显示全部楼层

【轉帖】

这工厂在31-3-15的账面价值是1.9 百万(2004年买价是2.3百万),在24-8-16 Ventana CoveringsSdn Bhd愿意以7.7百万向方案工程献购,再以28K 回租给方案工程。这个交易使方案工程净赚5.4百万或每股1.78分。

网站:

先介绍工厂,因为是要把飞机(公司)的轮胎(工厂)合理化。 2017现在和之后的运作将会是:“Revenue contribution from its lubrication productionarm, Solution Biogen Sdn Bhd, is also expected to double in FY15 as itrelocates its production facilities to a new plant in Bukit Kemuning, Shah Alamfrom Puchong.”

Company's new 35,000sq ft workshop will be operational by 2016 asconstruction work on it will begin soon. Wow.. Solution Biogen Sdn Bhd 12,658 SQ(原本Hangpalang in 1) to 35,000 sq ft newfactory ,对它有期待。

再看SEHB母公司。。新居不可能小过子公司吧? http://www.solutionholdings.com.my/InvestorRelation/ViewEvent.aspx

Wow ~ 果然劲,新厂在6-2-17动工了,三层楼面积43,560 sq ft(1 Acre)而且是在TPM.

看来林老板雄心勃勃,要成长。

在ACE版,方案工程一亿马币小公司,超强ROE。 灵魂人物: 创办人Lim YongHew 是董事经理,也是CEO(Chief Education Officer):)。

在他和团队的领导下财务报表会带来什么好数目?

7.7百万的小厂,2016年营业额35百万,净利7.7百万。 可以看得出,这家公司是靠创意和服务来建立生意,如果是环境造成瓶颈,那么充广是明智之举。 ROE 几多 ? EPS/NTA=3.09/12.24 = 25, 如果扣除现金6分(18652/304068),那么3.09/6.24 =49。果然是“吃脑”的精英团队。

很好奇,在股价已经翻了一番,冯大师还说可以买进?很少听过冯师父这么明显的叫买进指定公司的股。。 曾经庆幸和某某公司董事谈天, he said “Mr. Fong had approached to us…”。 这番话,让我忽然清醒,原来冯大师不止对财务报表严格,对管理层也是非常谨慎 ,会直接和管理层会谈。

2014 年是方案工程的转折点。相信ACQUISITION OF REMAINING STAKE (30%) INSOLUTION BIOFORCE SDN BHD是有相当的好处 。

*The acquisition willnot have any material effect on the earnings and EPS of the SEHB Group for theFYE 31 December 2013 and 2014 as the acquisition is completed in the fourthquarter of 2013.

在Current Ratio 方面,方案工程控制得很好,Current asset 是当前最高。 这就比如有六块钱现金应付负债的一块钱,在这里可以看得出营运方面相当轻松。

流动比率数目是六,但是和之前的“六”内涵是不一样的。

曾经和Petronas University(方案工程的重要客户之一)的内部承包商接触,现在国油集团开销谨慎,在节约开支,这个时期内部使用会尽量避开西方高价进口货,改用品质卓越的本地或区域的优良代替品。(这点可以在Petronas的财报看到), So…. 0093 现在确实是你天时地利,大展宏图的好时机。 虽然股价已经起了很多,但是相信今年开始方案工程将会是一家高成长的公司。 根据老板的意愿,希望可以2017年转主板。 我觉得投资某家基本面好的公司,需要的是基础上得付出努力研究报表,但最重要的是,再花上一点点的时间等待。我认为,心态决定成败。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 27-4-2017 06:07 PM

|

显示全部楼层

solutn:

solutn-wa:

|

|

|

|

|

|

|

|

|

|

|

|

发表于 28-4-2017 11:01 PM

|

显示全部楼层

solutn-wa:

某某著名部落格..

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

2995

2995  99

99