|

国家银行去年宣布,国内所有银行将在今年全面提升扣账卡(Debit Card)功能,即从今年1月开始,就以输入密码验证(PIN)取代签名付账方式,但签名过账方式还是会沿用至7月1日,好让持卡者能在新系统正式实行前有一段缓冲期。

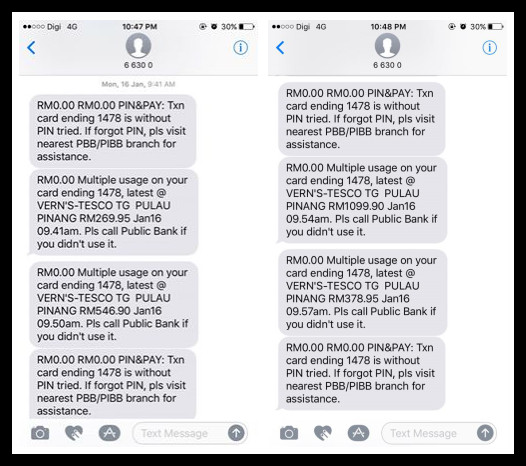

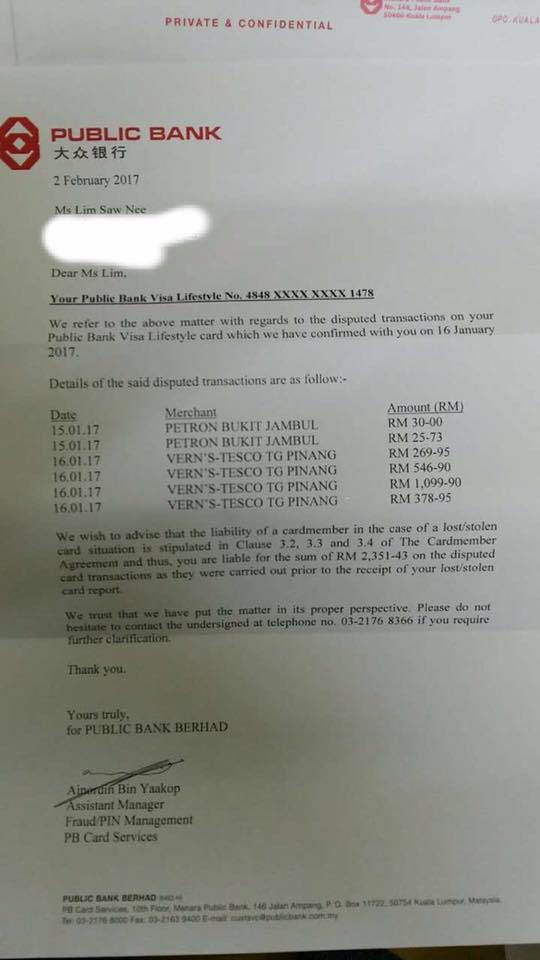

不过,过去也有不少网友指出,虽然手上的已经更新了,但有时候去买东西,商家还是一样没有要求输入密码,甚至也没有要求签名了,让人不禁担心手上的提款卡安全吗?  图片来源:截图自脸书 一名网友Sunny星期三(22日)在面子书发文投诉,自己的大众银行扣账卡遭人在15分钟内盗刷了两千多令吉。这名网友指出,由于她不知道自己的扣账卡不见了,因此没有致电银行马上停卡,就这样被人盗刷了。  图片来源:Sunny 脸书 Sunny指出,她在上个月16日突然收到信息,指她的卡在某特易购(Tesco)超市使用。当下,她赶紧请假去报警,同时到大众银行去投报。 “去到银行,银行职员告诉我,幸好我的钱还没过账,叫我回家等。查了之后,如果真的不是我用,就会还我。” Sunny在帖文中指出,回家后她也上网查了,发现交易真的是处于on hold(冻结)状态,隔天再查也是一样,但再隔一天却过账了。 “我马上打电话去问,结果他们告诉我,通过是正常的,叫我等他们查。”  图片来源:Sunny 脸书 没想到,大众银行在一个月后给她寄了一封信,指她必须负担全部责任,也就是盗刷的两千多令吉无法索回。

“真的不敢相信,我的提款卡竟然在15分钟内被盗刷了两千多,而且不用密码,也不用我的签名。” 有关帖文迅速引起疯传,《佳礼资讯网》也就此联系大众银行了解,是不是提款卡遭盗刷后只能自叹倒霉?提款卡又是不是可以在没有密码和签名的情况下使用呢? |

jackygogogogo 发表于 23-2-2017 07:19 PM

是不是可以把 limit set zero? 任何数目都需要输入密码才可过账

*provided the cardholders have not acted fraudulently or have not failed to inform the issuers as soon as reasonably practicable after having found that their debit card-i are lost or stolen.

BlazeA4 发表于 23-2-2017 07:59 PM

我早就说过了,用debitcard是最愚蠢最白痴的行为

wjleong15 发表于 23-2-2017 11:00 PM

如果没有理解错误

卡在手上

但是却在外面被盗刷是不需要负责的

如果卡遗失

但是迟了投保

期间被盗刷

是需要负责的

除非证明得到

通常成功例子不多

所以怀疑以上的问题1应该写反了

试想

如果人在马来 ...

本周最热文章

本周最热文章

ADVERTISEMENT

1411

1411

8

8